Warren Buffett famously said, ‘Volatility is far from synonymous with risk.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, Colfax Corporation (NYSE:CFX) does carry debt. But is this debt a concern to shareholders?

When Is Debt A Problem?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first step when considering a company’s debt levels is to consider its cash and debt together.

What Is Colfax’s Debt?

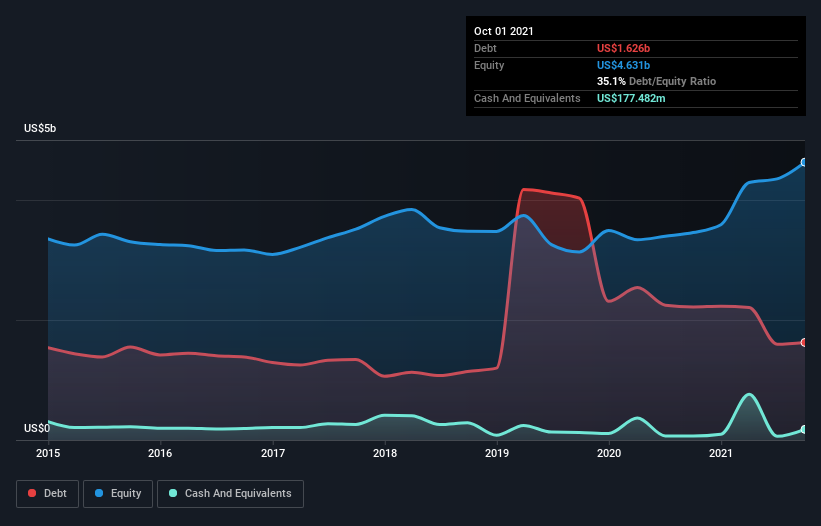

The image below, which you can click on for greater detail, shows that Colfax had debt of US$1.63b at the end of October 2021, a reduction from US$2.22b over a year. On the flip side, it has US$177.5m in cash leading to net debt of about US$1.45b.

How Strong Is Colfax’s Balance Sheet?

According to the last reported balance sheet, Colfax had liabilities of US$975.5m due within 12 months, and liabilities of US$2.37b due beyond 12 months. On the other hand, it had cash of US$177.5m and US$603.2m worth of receivables due within a year. So its liabilities total US$2.56b more than the combination of its cash and short-term receivables.

While this might seem like a lot, it is not so bad since Colfax has a market capitalization of US$7.81b, and so it could probably strengthen its balance sheet by raising capital if it needed to. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Colfax has a debt to EBITDA ratio of 2.5 and its EBIT covered its interest expense 3.8 times. Taken together this implies that, while we wouldn’t want to see debt levels rise, we think it can handle its current leverage. Also relevant is that Colfax has grown its EBIT by a very respectable 26% in the last year, thus enhancing its ability to pay down debt. There’s no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Colfax’s ability to maintain a healthy balance sheet going forward.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So we always check how much of that EBIT is translated into free cash flow. Over the most recent three years, Colfax recorded free cash flow worth 55% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This cold hard cash means it can reduce its debt when it wants to.

Our View

On our analysis Colfax’s EBIT growth rate should signal that it won’t have too much trouble with its debt. But the other factors we noted above weren’t so encouraging. For example, its interest cover makes us a little nervous about its debt. Considering this range of data points, we think Colfax is in a good position to manage its debt levels. Having said that, the load is sufficiently heavy that we would recommend any shareholders keep a close eye on it. The balance sheet is clearly the area to focus on when you are analysing debt.