Warren Buffett famously said, ‘Volatility is far from synonymous with risk.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We note that Falcon Minerals Corporation (NASDAQ:FLMN) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

What Risk Does Debt Bring?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first step when considering a company’s debt levels is to consider its cash and debt together.

What Is Falcon Minerals’s Net Debt?

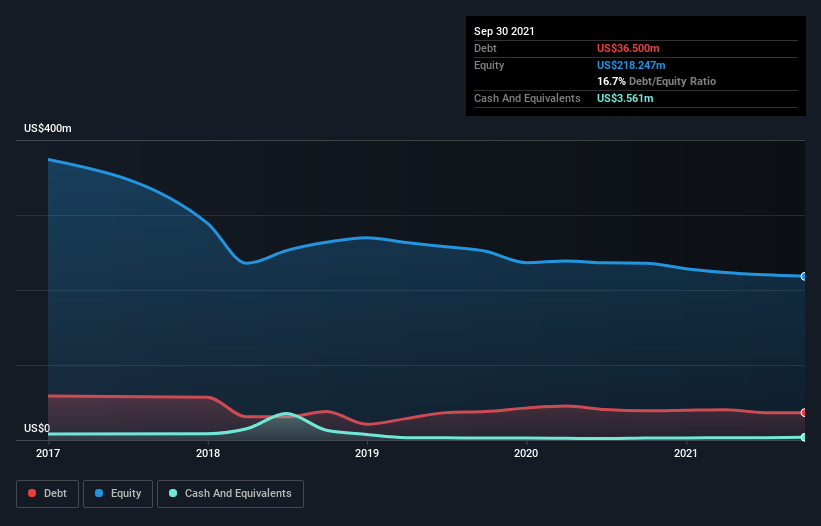

The image below, which you can click on for greater detail, shows that Falcon Minerals had debt of US$36.5m at the end of September 2021, a reduction from US$39.0m over a year. However, because it has a cash reserve of US$3.56m, its net debt is less, at about US$32.9m.

How Strong Is Falcon Minerals’ Balance Sheet?

We can see from the most recent balance sheet that Falcon Minerals had liabilities of US$7.92m falling due within a year, and liabilities of US$41.4m due beyond that. Offsetting this, it had US$3.56m in cash and US$9.58m in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$36.2m.

Given Falcon Minerals has a market capitalization of US$418.2m, it’s hard to believe these liabilities pose much threat. Having said that, it’s clear that we should continue to monitor its balance sheet, lest it change for the worse.

In order to size up a company’s debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Falcon Minerals’s net debt is only 0.83 times its EBITDA. And its EBIT easily covers its interest expense, being 12.8 times the size. So we’re pretty relaxed about its super-conservative use of debt. Even more impressive was the fact that Falcon Minerals grew its EBIT by 117% over twelve months. If maintained that growth will make the debt even more manageable in the years ahead. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Falcon Minerals’s ability to maintain a healthy balance sheet going forward.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So it’s worth checking how much of that EBIT is backed by free cash flow. Over the last three years, Falcon Minerals actually produced more free cash flow than EBIT. That sort of strong cash conversion gets us as excited as the crowd when the beat drops at a Daft Punk concert.

Our View

Happily, Falcon Minerals’s impressive interest cover implies it has the upper hand on its debt. And the good news does not stop there, as its conversion of EBIT to free cash flow also supports that impression! We think Falcon Minerals is no more beholden to its lenders, than the birds are to birdwatchers. For investing nerds like us its balance sheet is almost charming. There’s no doubt that we learn most about debt from the balance sheet.