Howard Marks put it nicely when he said that, rather than worrying about share price volatility, ‘The possibility of permanent loss is the risk I worry about… and every practical investor I know worries about.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, Sempra (NYSE:SRE) does carry debt. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first step when considering a company’s debt levels is to consider its cash and debt together.

How Much Debt Does Sempra Carry?

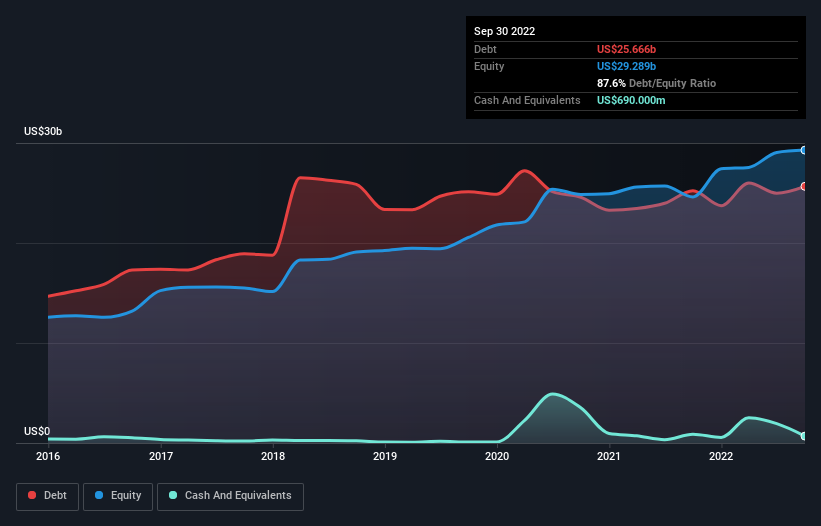

The chart below, which you can click on for greater detail, shows that Sempra had US$25.7b in debt in September 2022; about the same as the year before. However, because it has a cash reserve of US$690.0m, its net debt is less, at about US$25.0b.

How Strong Is Sempra’s Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Sempra had liabilities of US$7.84b due within 12 months and liabilities of US$38.4b due beyond that. Offsetting these obligations, it had cash of US$690.0m as well as receivables valued at US$2.33b due within 12 months. So its liabilities total US$43.3b more than the combination of its cash and short-term receivables.

This deficit is considerable relative to its very significant market capitalization of US$52.2b, so it does suggest shareholders should keep an eye on Sempra’s use of debt. Should its lenders demand that it shore up the balance sheet, shareholders would likely face severe dilution.

In order to size up a company’s debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Sempra’s debt is 5.0 times its EBITDA, and its EBIT cover its interest expense 2.7 times over. Taken together this implies that, while we wouldn’t want to see debt levels rise, we think it can handle its current leverage. On a slightly more positive note, Sempra grew its EBIT at 19% over the last year, further increasing its ability to manage debt. There’s no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Sempra can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So it’s worth checking how much of that EBIT is backed by free cash flow. During the last three years, Sempra burned a lot of cash. While investors are no doubt expecting a reversal of that situation in due course, it clearly does mean its use of debt is more risky.

Our View

We’d go so far as to say Sempra’s conversion of EBIT to free cash flow was disappointing. But on the bright side, its EBIT growth rate is a good sign, and makes us more optimistic. We should also note that Integrated Utilities industry companies like Sempra commonly do use debt without problems. Looking at the bigger picture, it seems clear to us that Sempra’s use of debt is creating risks for the company. If all goes well, that should boost returns, but on the flip side, the risk of permanent capital loss is elevated by the debt.