David Iben put it well when he said, ‘Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We note that Willdan Group, Inc. (NASDAQ:WLDN) does have debt on its balance sheet. But the more important question is: how much risk is that debt creating?

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

How Much Debt Does Willdan Group Carry?

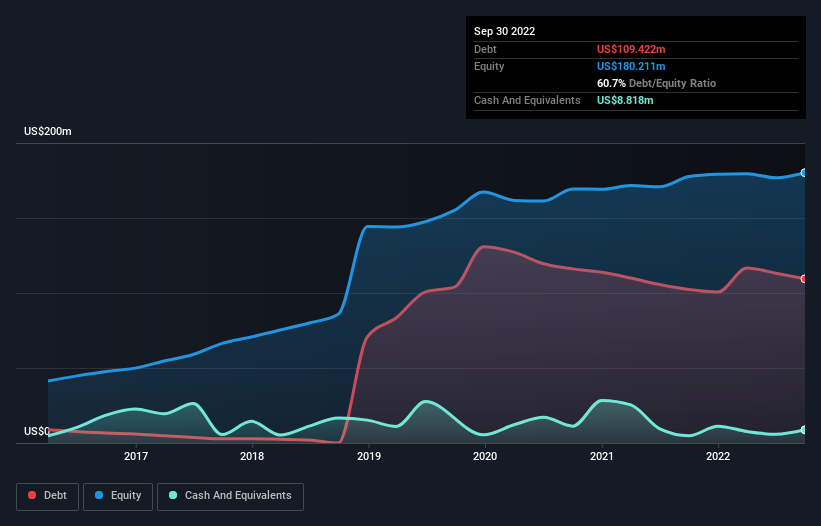

As you can see below, at the end of September 2022, Willdan Group had US$109.4m of debt, up from US$102.3m a year ago. Click the image for more detail. However, it also had US$8.82m in cash, and so its net debt is US$100.6m.

How Strong Is Willdan Group’s Balance Sheet?

We can see from the most recent balance sheet that Willdan Group had liabilities of US$110.5m falling due within a year, and liabilities of US$104.4m due beyond that. Offsetting these obligations, it had cash of US$8.82m as well as receivables valued at US$140.4m due within 12 months. So its liabilities total US$65.7m more than the combination of its cash and short-term receivables.

Willdan Group has a market capitalization of US$229.6m, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk. There’s no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Willdan Group’s ability to maintain a healthy balance sheet going forward.

In the last year Willdan Group wasn’t profitable at an EBIT level, but managed to grow its revenue by 14%, to US$408m. We usually like to see faster growth from unprofitable companies, but each to their own.

Caveat Emptor

Importantly, Willdan Group had an earnings before interest and tax (EBIT) loss over the last year. To be specific the EBIT loss came in at US$11m. When we look at that and recall the liabilities on its balance sheet, relative to cash, it seems unwise to us for the company to have any debt. So we think its balance sheet is a little strained, though not beyond repair. For example, we would not want to see a repeat of last year’s loss of US$8.9m. So to be blunt we do think it is risky.