Warren Buffett famously said, ‘Volatility is far from synonymous with risk.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. We can see that PVH Corp. (NYSE:PVH) does use debt in its business. But the more important question is: how much risk is that debt creating?

When Is Debt Dangerous?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

How Much Debt Does PVH Carry?

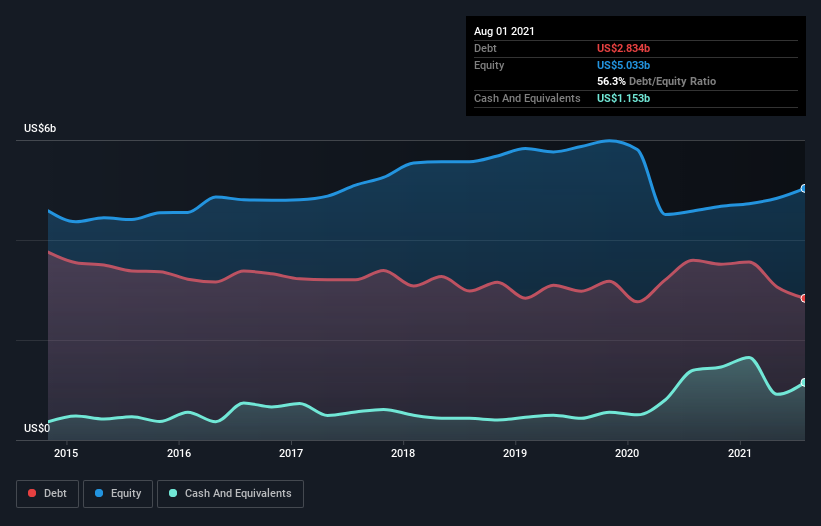

You can click the graphic below for the historical numbers, but it shows that PVH had US$2.83b of debt in August 2021, down from US$3.59b, one year before. However, because it has a cash reserve of US$1.15b, its net debt is less, at about US$1.68b.

A Look At PVH’s Liabilities

The latest balance sheet data shows that PVH had liabilities of US$2.53b due within a year, and liabilities of US$5.23b falling due after that. On the other hand, it had cash of US$1.15b and US$847.2m worth of receivables due within a year. So its liabilities total US$5.76b more than the combination of its cash and short-term receivables.

This deficit is considerable relative to its market capitalization of US$7.77b, so it does suggest shareholders should keep an eye on PVH’s use of debt. Should its lenders demand that it shore up the balance sheet, shareholders would likely face severe dilution.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

PVH has net debt worth 1.7 times EBITDA, which isn’t too much, but its interest cover looks a bit on the low side, with EBIT at only 5.4 times the interest expense. While that doesn’t worry us too much, it does suggest the interest payments are somewhat of a burden. Notably, PVH’s EBIT launched higher than Elon Musk, gaining a whopping 381% on last year. There’s no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if PVH can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So it’s worth checking how much of that EBIT is backed by free cash flow. Over the last three years, PVH recorded free cash flow worth a fulsome 97% of its EBIT, which is stronger than we’d usually expect. That puts it in a very strong position to pay down debt.

Our View

The good news is that PVH’s demonstrated ability to convert EBIT to free cash flow delights us like a fluffy puppy does a toddler. But truth be told we feel its level of total liabilities does undermine this impression a bit. Looking at all the aforementioned factors together, it strikes us that PVH can handle its debt fairly comfortably. On the plus side, this leverage can boost shareholder returns, but the potential downside is more risk of loss, so it’s worth monitoring the balance sheet. There’s no doubt that we learn most about debt from the balance sheet.