Warren Buffett famously said, ‘Volatility is far from synonymous with risk.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. We note that Royal Caribbean Cruises Ltd. (NYSE:RCL) does have debt on its balance sheet. But the more important question is: how much risk is that debt creating?

What Risk Does Debt Bring?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first step when considering a company’s debt levels is to consider its cash and debt together.

What Is Royal Caribbean Cruises’s Net Debt?

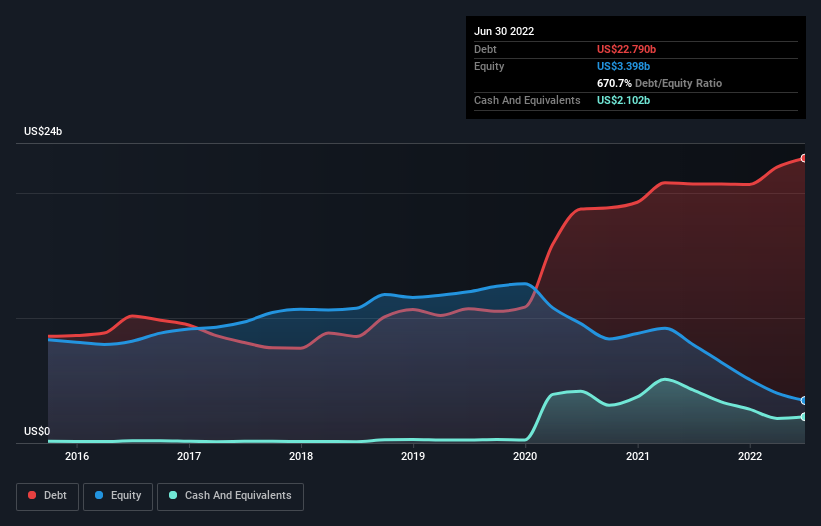

You can click the graphic below for the historical numbers, but it shows that as of June 2022 Royal Caribbean Cruises had US$22.8b of debt, an increase on US$20.7b, over one year. On the flip side, it has US$2.10b in cash leading to net debt of about US$20.7b.

How Healthy Is Royal Caribbean Cruises’ Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Royal Caribbean Cruises had liabilities of US$11.7b due within 12 months and liabilities of US$18.8b due beyond that. Offsetting these obligations, it had cash of US$2.10b as well as receivables valued at US$565.0m due within 12 months. So its liabilities total US$27.9b more than the combination of its cash and short-term receivables.

The deficiency here weighs heavily on the US$10.5b company itself, as if a child were struggling under the weight of an enormous back-pack full of books, his sports gear, and a trumpet. So we’d watch its balance sheet closely, without a doubt. At the end of the day, Royal Caribbean Cruises would probably need a major re-capitalization if its creditors were to demand repayment. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Royal Caribbean Cruises’s ability to maintain a healthy balance sheet going forward.

Over 12 months, Royal Caribbean Cruises reported revenue of US$4.7b, which is a gain of 4,915%, although it did not report any earnings before interest and tax. That’s virtually the hole-in-one of revenue growth!

Caveat Emptor

Despite the top line growth, Royal Caribbean Cruises still had an earnings before interest and tax (EBIT) loss over the last year. Indeed, it lost a very considerable US$3.1b at the EBIT level. Combining this information with the significant liabilities we already touched on makes us very hesitant about this stock, to say the least. That said, it is possible that the company will turn its fortunes around. But we think that is unlikely, given it is low on liquid assets, and burned through US$3.9b in the last year. So we think this stock is risky, like walking through a dirty dog park with a mask on.