David Iben put it well when he said, ‘Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. Importantly, X4 Pharmaceuticals, Inc. (NASDAQ:XFOR) does carry debt. But the more important question is: how much risk is that debt creating?

When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we think about a company’s use of debt, we first look at cash and debt together.

How Much Debt Does X4 Pharmaceuticals Carry?

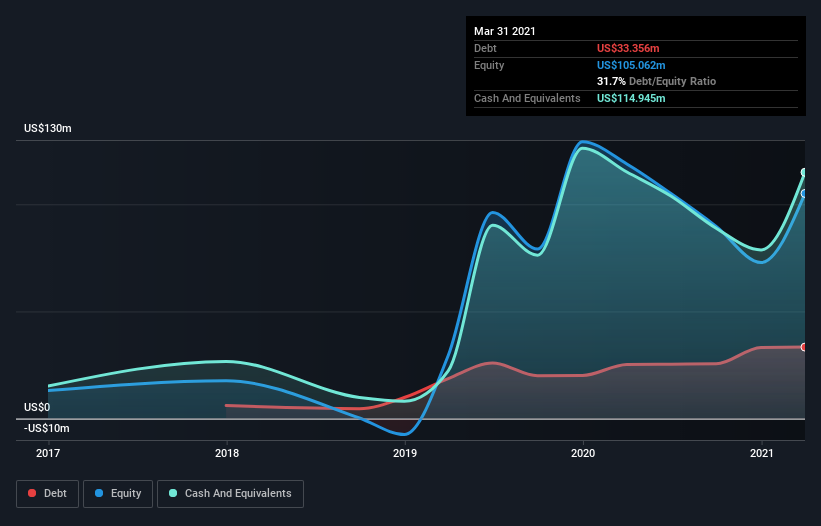

As you can see below, at the end of March 2021, X4 Pharmaceuticals had US$33.4m of debt, up from US$25.3m a year ago. Click the image for more detail. However, its balance sheet shows it holds US$114.9m in cash, so it actually has US$81.6m net cash.

How Healthy Is X4 Pharmaceuticals’ Balance Sheet?

Zooming in on the latest balance sheet data, we can see that X4 Pharmaceuticals had liabilities of US$14.7m due within 12 months and liabilities of US$41.3m due beyond that. Offsetting this, it had US$114.9m in cash and US$768.0k in receivables that were due within 12 months. So it actually has US$59.7m more liquid assets than total liabilities.

This luscious liquidity implies that X4 Pharmaceuticals’ balance sheet is sturdy like a giant sequoia tree. On this view, lenders should feel as safe as the beloved of a black-belt karate master. Succinctly put, X4 Pharmaceuticals boasts net cash, so it’s fair to say it does not have a heavy debt load! The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if X4 Pharmaceuticals can strengthen its balance sheet over time.

Given its lack of meaningful operating revenue, X4 Pharmaceuticals shareholders no doubt hope it can fund itself until it has a profitable product.

So How Risky Is X4 Pharmaceuticals?

By their very nature companies that are losing money are more risky than those with a long history of profitability. And in the last year X4 Pharmaceuticals had an earnings before interest and tax (EBIT) loss, truth be told. And over the same period it saw negative free cash outflow of US$63m and booked a US$78m accounting loss. But at least it has US$81.6m on the balance sheet to spend on growth, near-term. Even though its balance sheet seems sufficiently liquid, debt always makes us a little nervous if a company doesn’t produce free cash flow regularly. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet – far from it.