Legendary fund manager Li Lu (who Charlie Munger backed) once said, ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We note that IQVIA Holdings Inc. (NYSE:IQV) does have debt on its balance sheet. But should shareholders be worried about its use of debt?

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

What Is IQVIA Holdings’s Net Debt?

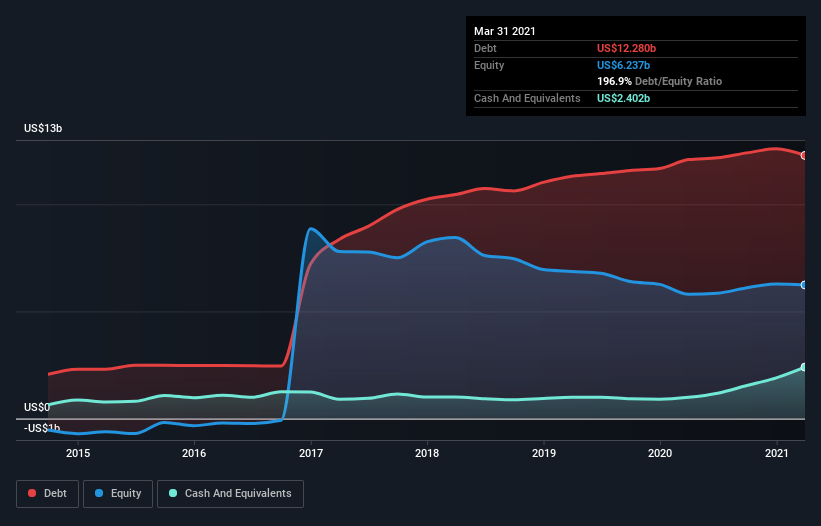

As you can see below, IQVIA Holdings had US$12.1b of debt, at March 2021, which is about the same as the year before. You can click the chart for greater detail. On the flip side, it has US$2.40b in cash leading to net debt of about US$9.72b.

A Look At IQVIA Holdings’ Liabilities

The latest balance sheet data shows that IQVIA Holdings had liabilities of US$4.87b due within a year, and liabilities of US$13.4b falling due after that. On the other hand, it had cash of US$2.40b and US$2.43b worth of receivables due within a year. So it has liabilities totalling US$13.4b more than its cash and near-term receivables, combined.

This deficit isn’t so bad because IQVIA Holdings is worth a massive US$47.7b, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. But it’s clear that we should definitely closely examine whether it can manage its debt without dilution.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

While IQVIA Holdings’s debt to EBITDA ratio (4.9) suggests that it uses some debt, its interest cover is very weak, at 2.4, suggesting high leverage. It seems that the business incurs large depreciation and amortisation charges, so maybe its debt load is heavier than it would first appear, since EBITDA is arguably a generous measure of earnings. So shareholders should probably be aware that interest expenses appear to have really impacted the business lately. However, one redeeming factor is that IQVIA Holdings grew its EBIT at 11% over the last 12 months, boosting its ability to handle its debt. There’s no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if IQVIA Holdings can strengthen its balance sheet over time.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So we always check how much of that EBIT is translated into free cash flow. Happily for any shareholders, IQVIA Holdings actually produced more free cash flow than EBIT over the last three years. There’s nothing better than incoming cash when it comes to staying in your lenders’ good graces.

Our View

When it comes to the balance sheet, the standout positive for IQVIA Holdings was the fact that it seems able to convert EBIT to free cash flow confidently. But the other factors we noted above weren’t so encouraging. In particular, net debt to EBITDA gives us cold feet. Considering this range of data points, we think IQVIA Holdings is in a good position to manage its debt levels. But a word of caution: we think debt levels are high enough to justify ongoing monitoring. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet.