Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that ‘Volatility is far from synonymous with risk.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. Importantly, The Southern Company (NYSE:SO) does carry debt. But should shareholders be worried about its use of debt?

What Risk Does Debt Bring?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

What Is Southern’s Net Debt?

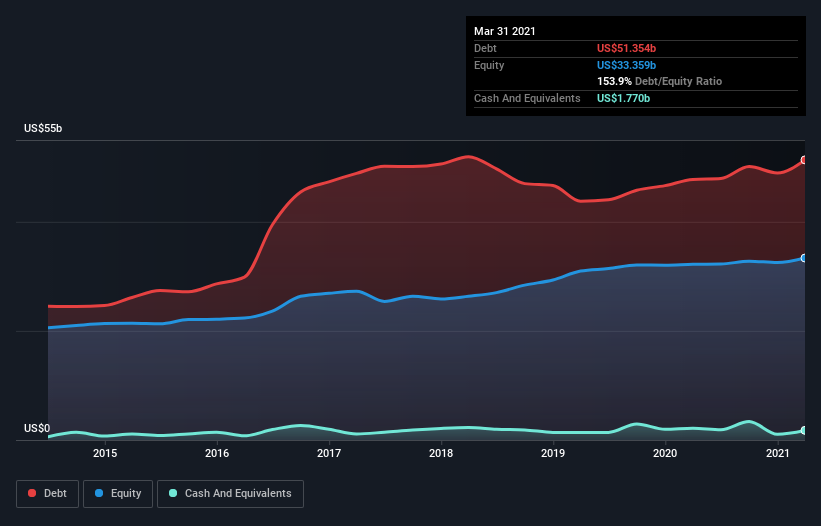

The image below, which you can click on for greater detail, shows that at March 2021 Southern had debt of US$51.4b, up from US$47.8b in one year. However, because it has a cash reserve of US$1.77b, its net debt is less, at about US$49.6b.

How Strong Is Southern’s Balance Sheet?

The latest balance sheet data shows that Southern had liabilities of US$11.6b due within a year, and liabilities of US$80.4b falling due after that. On the other hand, it had cash of US$1.77b and US$3.03b worth of receivables due within a year. So its liabilities total US$87.2b more than the combination of its cash and short-term receivables.

When you consider that this deficiency exceeds the company’s huge US$65.7b market capitalization, you might well be inclined to review the balance sheet intently. In the scenario where the company had to clean up its balance sheet quickly, it seems likely shareholders would suffer extensive dilution.

In order to size up a company’s debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

With a net debt to EBITDA ratio of 5.2, it’s fair to say Southern does have a significant amount of debt. But the good news is that it boasts fairly comforting interest cover of 3.1 times, suggesting it can responsibly service its obligations. Notably, Southern’s EBIT was pretty flat over the last year, which isn’t ideal given the debt load. There’s no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Southern can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. During the last three years, Southern burned a lot of cash. While investors are no doubt expecting a reversal of that situation in due course, it clearly does mean its use of debt is more risky.

Our View

To be frank both Southern’s net debt to EBITDA and its track record of converting EBIT to free cash flow make us rather uncomfortable with its debt levels. But at least its EBIT growth rate is not so bad. It’s also worth noting that Southern is in the Electric Utilities industry, which is often considered to be quite defensive. After considering the datapoints discussed, we think Southern has too much debt. That sort of riskiness is ok for some, but it certainly doesn’t float our boat. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet – far from it.