Legendary fund manager Li Lu (who Charlie Munger backed) once said, ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that Studio City International Holdings Limited (NYSE:MSC) does use debt in its business. But should shareholders be worried about its use of debt?

When Is Debt A Problem?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. When we examine debt levels, we first consider both cash and debt levels, together.

How Much Debt Does Studio City International Holdings Carry?

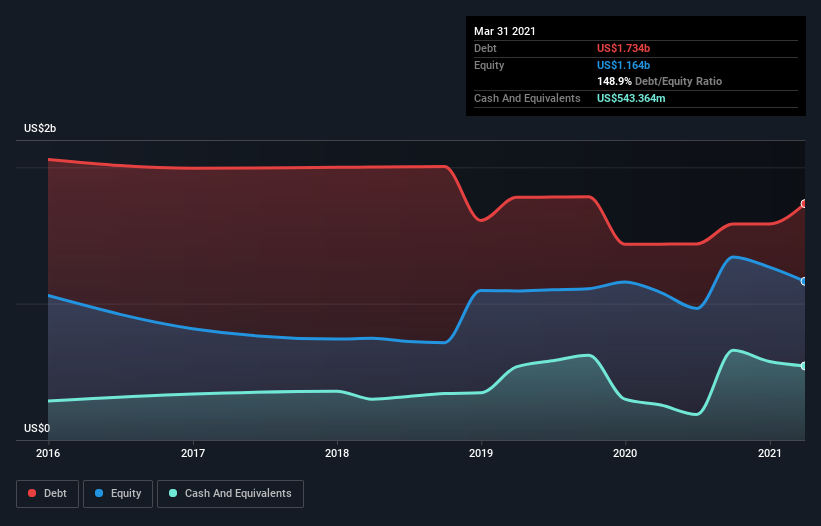

You can click the graphic below for the historical numbers, but it shows that as of March 2021 Studio City International Holdings had US$1.73b of debt, an increase on US$1.44b, over one year. On the flip side, it has US$543.4m in cash leading to net debt of about US$1.19b.

How Healthy Is Studio City International Holdings’ Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Studio City International Holdings had liabilities of US$119.5m due within 12 months and liabilities of US$1.77b due beyond that. Offsetting these obligations, it had cash of US$543.4m as well as receivables valued at US$13.1m due within 12 months. So its liabilities total US$1.33b more than the combination of its cash and short-term receivables.

When you consider that this deficiency exceeds the company’s US$1.32b market capitalization, you might well be inclined to review the balance sheet intently. Hypothetically, extremely heavy dilution would be required if the company were forced to pay down its liabilities by raising capital at the current share price. There’s no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Studio City International Holdings can strengthen its balance sheet over time.

In the last year Studio City International Holdings had a loss before interest and tax, and actually shrunk its revenue by 92%, to US$41m. To be frank that doesn’t bode well.

Caveat Emptor

While Studio City International Holdings’s falling revenue is about as heartwarming as a wet blanket, arguably its earnings before interest and tax (EBIT) loss is even less appealing. Indeed, it lost a very considerable US$258m at the EBIT level. When we look at that alongside the significant liabilities, we’re not particularly confident about the company. We’d want to see some strong near-term improvements before getting too interested in the stock. Not least because it had negative free cash flow of US$370m over the last twelve months. So suffice it to say we consider the stock to be risky. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet.