Legendary fund manager Li Lu (who Charlie Munger backed) once said, ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. Importantly, LGI Homes, Inc. (NASDAQ:LGIH) does carry debt. But is this debt a concern to shareholders?

Why Does Debt Bring Risk?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

What Is LGI Homes’s Net Debt?

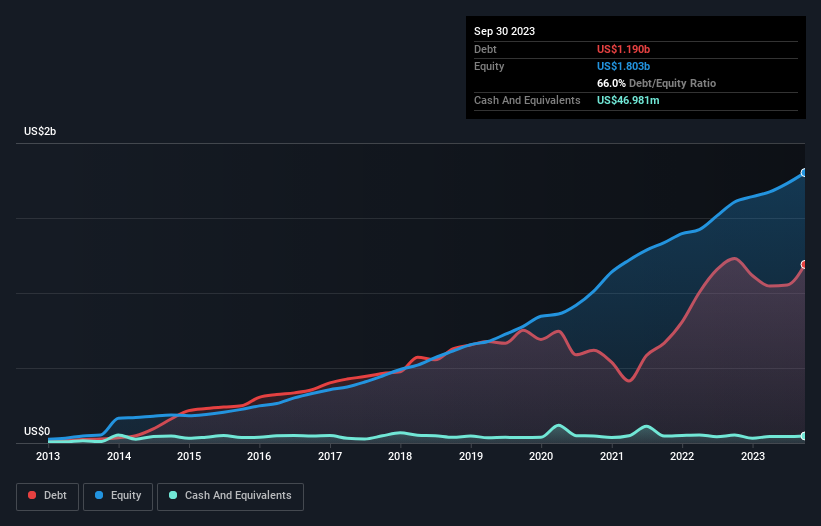

The chart below, which you can click on for greater detail, shows that LGI Homes had US$1.19b in debt in September 2023; about the same as the year before. However, it does have US$47.0m in cash offsetting this, leading to net debt of about US$1.14b.

A Look At LGI Homes’ Liabilities

According to the last reported balance sheet, LGI Homes had liabilities of US$120.9m due within 12 months, and liabilities of US$1.41b due beyond 12 months. Offsetting these obligations, it had cash of US$47.0m as well as receivables valued at US$35.7m due within 12 months. So it has liabilities totalling US$1.45b more than its cash and near-term receivables, combined.

While this might seem like a lot, it is not so bad since LGI Homes has a market capitalization of US$2.89b, and so it could probably strengthen its balance sheet by raising capital if it needed to. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk.

In order to size up a company’s debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

As it happens LGI Homes has a fairly concerning net debt to EBITDA ratio of 5.1 but very strong interest coverage of 1k. This means that unless the company has access to very cheap debt, that interest expense will likely grow in the future. Shareholders should be aware that LGI Homes’s EBIT was down 56% last year. If that decline continues then paying off debt will be harder than selling foie gras at a vegan convention. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if LGI Homes can strengthen its balance sheet over time.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So we always check how much of that EBIT is translated into free cash flow. During the last three years, LGI Homes burned a lot of cash. While that may be a result of expenditure for growth, it does make the debt far more risky.

Our View

On the face of it, LGI Homes’s conversion of EBIT to free cash flow left us tentative about the stock, and its EBIT growth rate was no more enticing than the one empty restaurant on the busiest night of the year. But at least it’s pretty decent at covering its interest expense with its EBIT; that’s encouraging. We’re quite clear that we consider LGI Homes to be really rather risky, as a result of its balance sheet health. For this reason we’re pretty cautious about the stock, and we think shareholders should keep a close eye on its liquidity. When analysing debt levels, the balance sheet is the obvious place to start.