Warren Buffett famously said, ‘Volatility is far from synonymous with risk.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We can see that Eastman Kodak Company (NYSE:KODK) does use debt in its business. But is this debt a concern to shareholders?

Why Does Debt Bring Risk?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first step when considering a company’s debt levels is to consider its cash and debt together.

What Is Eastman Kodak’s Debt?

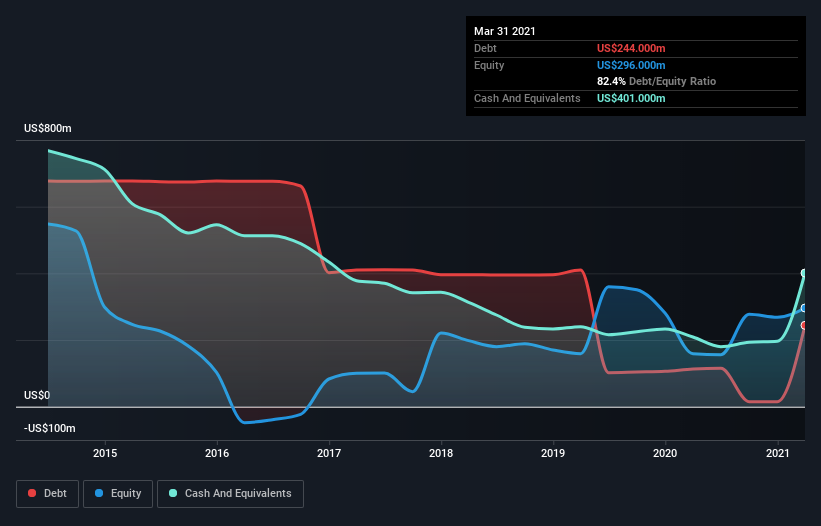

You can click the graphic below for the historical numbers, but it shows that as of March 2021 Eastman Kodak had US$244.0m of debt, an increase on US$113.0m, over one year. However, its balance sheet shows it holds US$401.0m in cash, so it actually has US$157.0m net cash.

How Healthy Is Eastman Kodak’s Balance Sheet?

We can see from the most recent balance sheet that Eastman Kodak had liabilities of US$295.0m falling due within a year, and liabilities of US$898.0m due beyond that. On the other hand, it had cash of US$401.0m and US$166.0m worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$626.0m.

This deficit is considerable relative to its market capitalization of US$691.6m, so it does suggest shareholders should keep an eye on Eastman Kodak’s use of debt. Should its lenders demand that it shore up the balance sheet, shareholders would likely face severe dilution. Despite its noteworthy liabilities, Eastman Kodak boasts net cash, so it’s fair to say it does not have a heavy debt load!

Importantly, Eastman Kodak’s EBIT fell a jaw-dropping 29% in the last twelve months. If that earnings trend continues then paying off its debt will be about as easy as herding cats on to a roller coaster. The balance sheet is clearly the area to focus on when you are analysing debt. But you can’t view debt in total isolation; since Eastman Kodak will need earnings to service that debt.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. Eastman Kodak may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. During the last three years, Eastman Kodak burned a lot of cash. While investors are no doubt expecting a reversal of that situation in due course, it clearly does mean its use of debt is more risky.

Summing up

Although Eastman Kodak’s balance sheet isn’t particularly strong, due to the total liabilities, it is clearly positive to see that it has net cash of US$157.0m. Unfortunately, though, both its struggle EBIT growth rate and its conversion of EBIT to free cash flow leave us concerned about Eastman Kodak So even though it has net cash, we do think the business has some risks worth watching. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet.