The external fund manager backed by Berkshire Hathaway’s Charlie Munger, Li Lu, makes no bones about it when he says ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. As with many other companies Gibraltar Industries, Inc. (NASDAQ:ROCK) makes use of debt. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first step when considering a company’s debt levels is to consider its cash and debt together.

What Is Gibraltar Industries’s Debt?

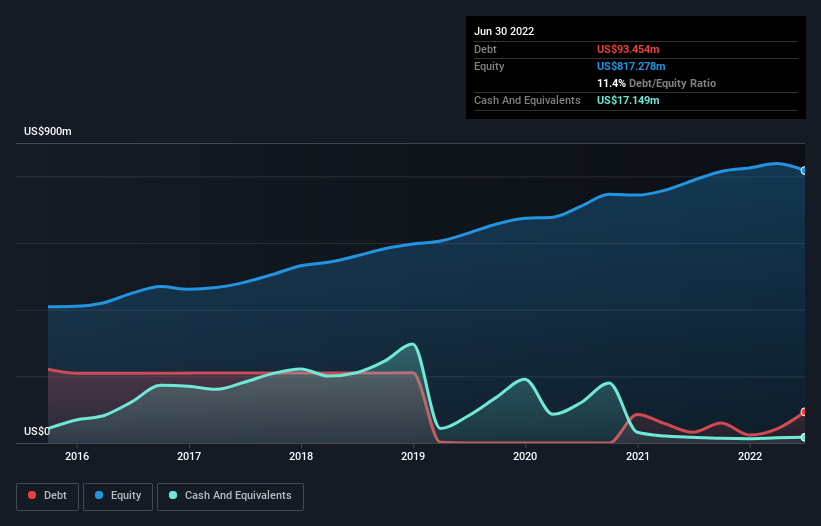

As you can see below, at the end of June 2022, Gibraltar Industries had US$93.5m of debt, up from US$32.3m a year ago. Click the image for more detail. However, it does have US$17.1m in cash offsetting this, leading to net debt of about US$76.3m.

How Strong Is Gibraltar Industries’ Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Gibraltar Industries had liabilities of US$303.5m due within 12 months and liabilities of US$174.6m due beyond that. On the other hand, it had cash of US$17.1m and US$275.6m worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$185.4m.

Given Gibraltar Industries has a market capitalization of US$1.31b, it’s hard to believe these liabilities pose much threat. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Gibraltar Industries has a low net debt to EBITDA ratio of only 0.49. And its EBIT easily covers its interest expense, being 61.2 times the size. So we’re pretty relaxed about its super-conservative use of debt. Fortunately, Gibraltar Industries grew its EBIT by 8.4% in the last year, making that debt load look even more manageable. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Gibraltar Industries’s ability to maintain a healthy balance sheet going forward.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So it’s worth checking how much of that EBIT is backed by free cash flow. During the last three years, Gibraltar Industries produced sturdy free cash flow equating to 56% of its EBIT, about what we’d expect. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Our View

The good news is that Gibraltar Industries’s demonstrated ability to cover its interest expense with its EBIT delights us like a fluffy puppy does a toddler. And that’s just the beginning of the good news since its net debt to EBITDA is also very heartening. Taking all this data into account, it seems to us that Gibraltar Industries takes a pretty sensible approach to debt. While that brings some risk, it can also enhance returns for shareholders.