The external fund manager backed by Berkshire Hathaway’s Charlie Munger, Li Lu, makes no bones about it when he says ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. As with many other companies Enterprise Group, Inc. (TSE:E) makes use of debt. But the more important question is: how much risk is that debt creating?

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we examine debt levels, we first consider both cash and debt levels, together.

How Much Debt Does Enterprise Group Carry?

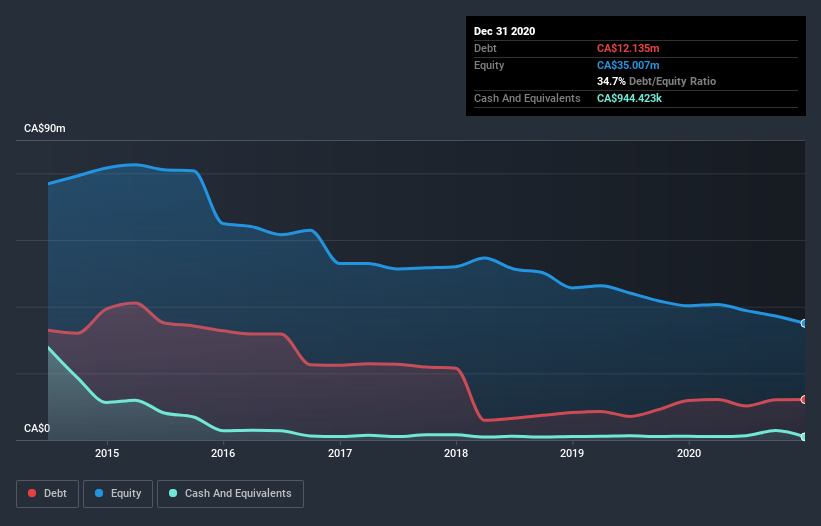

The chart below, which you can click on for greater detail, shows that Enterprise Group had CA$12.1m in debt in December 2020; about the same as the year before. However, because it has a cash reserve of CA$944.4k, its net debt is less, at about CA$11.2m.

How Strong Is Enterprise Group’s Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Enterprise Group had liabilities of CA$2.58m due within 12 months and liabilities of CA$14.7m due beyond that. On the other hand, it had cash of CA$944.4k and CA$4.17m worth of receivables due within a year. So its liabilities total CA$12.1m more than the combination of its cash and short-term receivables.

When you consider that this deficiency exceeds the company’s CA$8.83m market capitalization, you might well be inclined to review the balance sheet intently. In the scenario where the company had to clean up its balance sheet quickly, it seems likely shareholders would suffer extensive dilution. There’s no doubt that we learn most about debt from the balance sheet. But it is Enterprise Group’s earnings that will influence how the balance sheet holds up in the future. So when considering debt, it’s definitely worth looking at the earnings trend.

Over 12 months, Enterprise Group made a loss at the EBIT level, and saw its revenue drop to CA$16m, which is a fall of 20%. To be frank that doesn’t bode well.

Caveat Emptor

While Enterprise Group’s falling revenue is about as heartwarming as a wet blanket, arguably its earnings before interest and tax (EBIT) loss is even less appealing. Indeed, it lost CA$644k at the EBIT level. Considering that alongside the liabilities mentioned above make us nervous about the company. We’d want to see some strong near-term improvements before getting too interested in the stock. For example, we would not want to see a repeat of last year’s loss of CA$4.4m. In the meantime, we consider the stock to be risky. There’s no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet – far from it.