Warren Buffett famously said, ‘Volatility is far from synonymous with risk.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We note that Tri Pointe Homes, Inc. (NYSE:TPH) does have debt on its balance sheet. But is this debt a concern to shareholders?

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first step when considering a company’s debt levels is to consider its cash and debt together.

How Much Debt Does Tri Pointe Homes Carry?

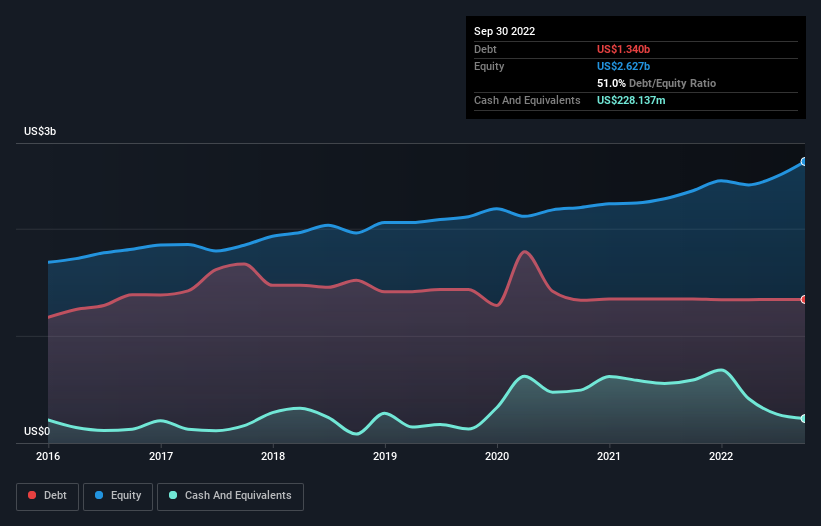

As you can see below, Tri Pointe Homes had US$1.34b of debt, at September 2022, which is about the same as the year before. You can click the chart for greater detail. However, it also had US$228.1m in cash, and so its net debt is US$1.11b.

A Look At Tri Pointe Homes’ Liabilities

We can see from the most recent balance sheet that Tri Pointe Homes had liabilities of US$264.8m falling due within a year, and liabilities of US$1.63b due beyond that. Offsetting these obligations, it had cash of US$228.1m as well as receivables valued at US$67.2m due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$1.60b.

This is a mountain of leverage relative to its market capitalization of US$1.89b. Should its lenders demand that it shore up the balance sheet, shareholders would likely face severe dilution.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Tri Pointe Homes’s net debt is only 1.5 times its EBITDA. And its EBIT covers its interest expense a whopping 1k times over. So we’re pretty relaxed about its super-conservative use of debt. Also positive, Tri Pointe Homes grew its EBIT by 23% in the last year, and that should make it easier to pay down debt, going forward. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Tri Pointe Homes’s ability to maintain a healthy balance sheet going forward.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So it’s worth checking how much of that EBIT is backed by free cash flow. During the last three years, Tri Pointe Homes produced sturdy free cash flow equating to 67% of its EBIT, about what we’d expect. This cold hard cash means it can reduce its debt when it wants to.

Our View

Happily, Tri Pointe Homes’s impressive interest cover implies it has the upper hand on its debt. But, on a more sombre note, we are a little concerned by its level of total liabilities. Looking at all the aforementioned factors together, it strikes us that Tri Pointe Homes can handle its debt fairly comfortably. Of course, while this leverage can enhance returns on equity, it does bring more risk, so it’s worth keeping an eye on this one.