Warren Buffett famously said, ‘Volatility is far from synonymous with risk.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. As with many other companies DexCom, Inc. (NASDAQ:DXCM) makes use of debt. But the more important question is: how much risk is that debt creating?

When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we think about a company’s use of debt, we first look at cash and debt together.

What Is DexCom’s Net Debt?

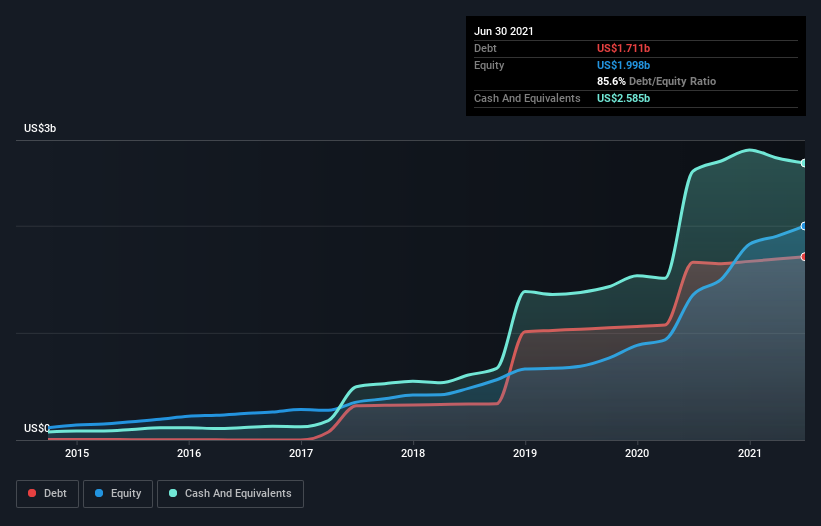

As you can see below, DexCom had US$1.71b of debt, at June 2021, which is about the same as the year before. You can click the chart for greater detail. But it also has US$2.58b in cash to offset that, meaning it has US$874.2m net cash.

How Healthy Is DexCom’s Balance Sheet?

According to the last reported balance sheet, DexCom had liabilities of US$600.7m due within 12 months, and liabilities of US$1.91b due beyond 12 months. Offsetting these obligations, it had cash of US$2.58b as well as receivables valued at US$483.5m due within 12 months. So it can boast US$562.2m more liquid assets than total liabilities.

Having regard to DexCom’s size, it seems that its liquid assets are well balanced with its total liabilities. So it’s very unlikely that the US$53.2b company is short on cash, but still worth keeping an eye on the balance sheet. Succinctly put, DexCom boasts net cash, so it’s fair to say it does not have a heavy debt load!

It is well worth noting that DexCom’s EBIT shot up like bamboo after rain, gaining 33% in the last twelve months. That’ll make it easier to manage its debt. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine DexCom’s ability to maintain a healthy balance sheet going forward.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. DexCom may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. During the last three years, DexCom produced sturdy free cash flow equating to 53% of its EBIT, about what we’d expect. This cold hard cash means it can reduce its debt when it wants to.

Summing up

While it is always sensible to investigate a company’s debt, in this case DexCom has US$874.2m in net cash and a decent-looking balance sheet. And it impressed us with its EBIT growth of 33% over the last year. So we don’t think DexCom’s use of debt is risky. When analysing debt levels, the balance sheet is the obvious place to start.