Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that ‘Volatility is far from synonymous with risk.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. As with many other companies NexTier Oilfield Solutions Inc. (NYSE:NEX) makes use of debt. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

What Is NexTier Oilfield Solutions’s Debt?

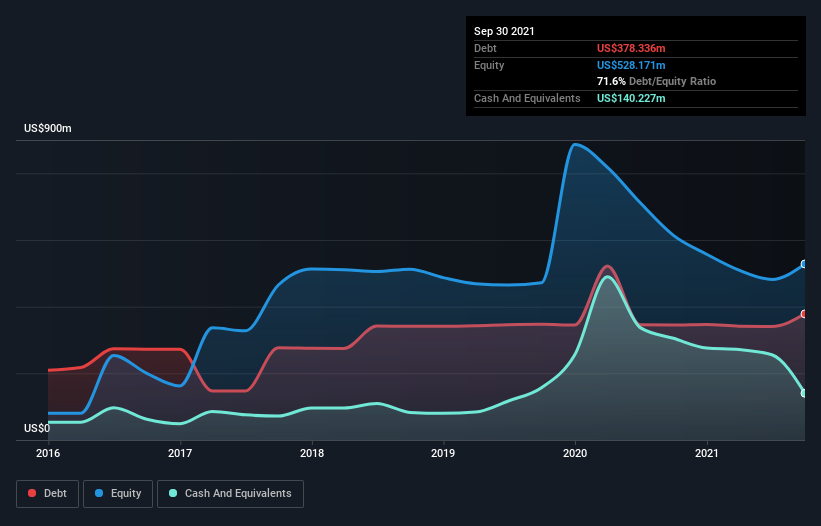

The image below, which you can click on for greater detail, shows that at September 2021 NexTier Oilfield Solutions had debt of US$378.3m, up from US$344.8m in one year. On the flip side, it has US$140.2m in cash leading to net debt of about US$238.1m.

A Look At NexTier Oilfield Solutions’ Liabilities

Zooming in on the latest balance sheet data, we can see that NexTier Oilfield Solutions had liabilities of US$461.6m due within 12 months and liabilities of US$428.2m due beyond that. Offsetting this, it had US$140.2m in cash and US$265.4m in receivables that were due within 12 months. So it has liabilities totalling US$484.2m more than its cash and near-term receivables, combined.

While this might seem like a lot, it is not so bad since NexTier Oilfield Solutions has a market capitalization of US$1.52b, and so it could probably strengthen its balance sheet by raising capital if it needed to. But it’s clear that we should definitely closely examine whether it can manage its debt without dilution. There’s no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine NexTier Oilfield Solutions’s ability to maintain a healthy balance sheet going forward.

In the last year NexTier Oilfield Solutions had a loss before interest and tax, and actually shrunk its revenue by 26%, to US$1.1b. To be frank that doesn’t bode well.

Caveat Emptor

Not only did NexTier Oilfield Solutions’s revenue slip over the last twelve months, but it also produced negative earnings before interest and tax (EBIT). Its EBIT loss was a whopping US$190m. Considering that alongside the liabilities mentioned above does not give us much confidence that company should be using so much debt. Quite frankly we think the balance sheet is far from match-fit, although it could be improved with time. However, it doesn’t help that it burned through US$189m of cash over the last year. So in short it’s a really risky stock.