Legendary fund manager Li Lu (who Charlie Munger backed) once said, ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. Importantly, NIO Inc. (NYSE:NIO) does carry debt. But the more important question is: how much risk is that debt creating?

What Risk Does Debt Bring?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

What Is NIO’s Debt?

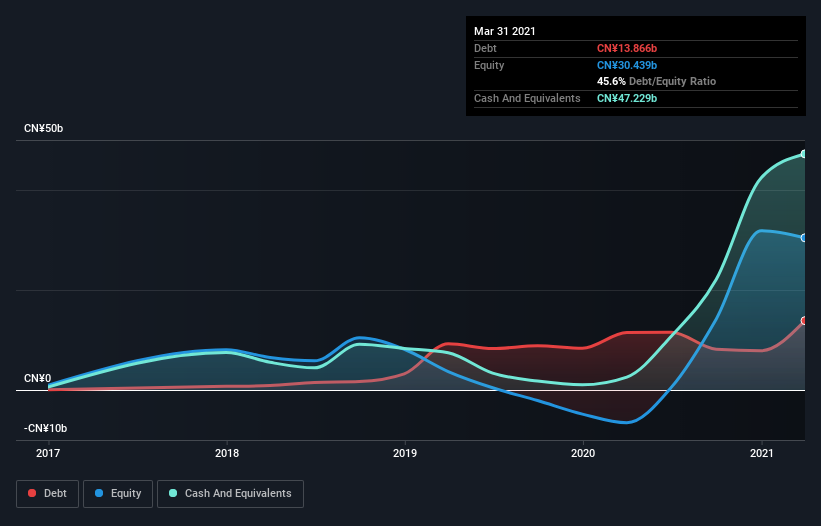

As you can see below, at the end of March 2021, NIO had CN¥13.9b of debt, up from CN¥11.5b a year ago. Click the image for more detail. However, it does have CN¥47.2b in cash offsetting this, leading to net cash of CN¥33.4b.

How Strong Is NIO’s Balance Sheet?

We can see from the most recent balance sheet that NIO had liabilities of CN¥17.0b falling due within a year, and liabilities of CN¥13.6b due beyond that. On the other hand, it had cash of CN¥47.2b and CN¥1.68b worth of receivables due within a year. So it can boast CN¥18.2b more liquid assets than total liabilities.

This short term liquidity is a sign that NIO could probably pay off its debt with ease, as its balance sheet is far from stretched. Simply put, the fact that NIO has more cash than debt is arguably a good indication that it can manage its debt safely. There’s no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if NIO can strengthen its balance sheet over time.

In the last year NIO wasn’t profitable at an EBIT level, but managed to grow its revenue by 202%, to CN¥23b. That’s virtually the hole-in-one of revenue growth!

So How Risky Is NIO?

Although NIO had an earnings before interest and tax (EBIT) loss over the last twelve months, it generated positive free cash flow of CN¥823m. So taking that on face value, and considering the net cash situation, we don’t think that the stock is too risky in the near term. We think its revenue growth of 202% is a good sign. We’d see further strong growth as an optimistic indication. There’s no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet.