David Iben put it well when he said, ‘Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. Importantly, AMN Healthcare Services, Inc. (NYSE:AMN) does carry debt. But the more important question is: how much risk is that debt creating?

When Is Debt Dangerous?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we think about a company’s use of debt, we first look at cash and debt together.

What Is AMN Healthcare Services’s Debt?

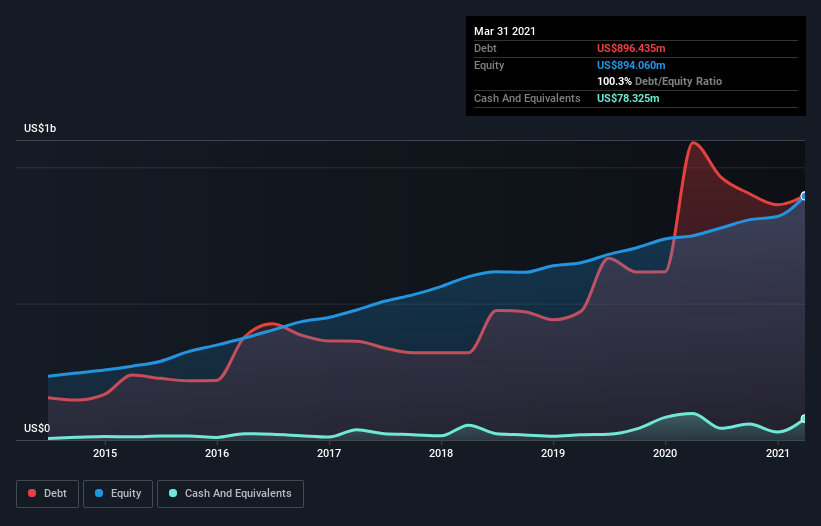

You can click the graphic below for the historical numbers, but it shows that AMN Healthcare Services had US$896.4m of debt in March 2021, down from US$1.09b, one year before. However, because it has a cash reserve of US$78.3m, its net debt is less, at about US$818.1m.

How Healthy Is AMN Healthcare Services’ Balance Sheet?

The latest balance sheet data shows that AMN Healthcare Services had liabilities of US$599.0m due within a year, and liabilities of US$1.15b falling due after that. Offsetting these obligations, it had cash of US$78.3m as well as receivables valued at US$700.5m due within 12 months. So it has liabilities totalling US$970.2m more than its cash and near-term receivables, combined.

While this might seem like a lot, it is not so bad since AMN Healthcare Services has a market capitalization of US$4.37b, and so it could probably strengthen its balance sheet by raising capital if it needed to. However, it is still worthwhile taking a close look at its ability to pay off debt.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

AMN Healthcare Services has net debt worth 2.5 times EBITDA, which isn’t too much, but its interest cover looks a bit on the low side, with EBIT at only 4.2 times the interest expense. While these numbers do not alarm us, it’s worth noting that the cost of the company’s debt is having a real impact. Importantly, AMN Healthcare Services grew its EBIT by 33% over the last twelve months, and that growth will make it easier to handle its debt. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine AMN Healthcare Services’s ability to maintain a healthy balance sheet going forward.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So it’s worth checking how much of that EBIT is backed by free cash flow. During the last three years, AMN Healthcare Services generated free cash flow amounting to a very robust 93% of its EBIT, more than we’d expect. That puts it in a very strong position to pay down debt.

Our View

The good news is that AMN Healthcare Services’s demonstrated ability to convert EBIT to free cash flow delights us like a fluffy puppy does a toddler. But truth be told we feel its interest cover does undermine this impression a bit. We would also note that Healthcare industry companies like AMN Healthcare Services commonly do use debt without problems. Zooming out, AMN Healthcare Services seems to use debt quite reasonably; and that gets the nod from us. While debt does bring risk, when used wisely it can also bring a higher return on equity. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. These risks can be hard to spot.