Legendary fund manager Li Lu (who Charlie Munger backed) once said, ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We can see that The Coca-Cola Company (NYSE:KO) does use debt in its business. But is this debt a concern to shareholders?

Why Does Debt Bring Risk?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we think about a company’s use of debt, we first look at cash and debt together.

How Much Debt Does Coca-Cola Carry?

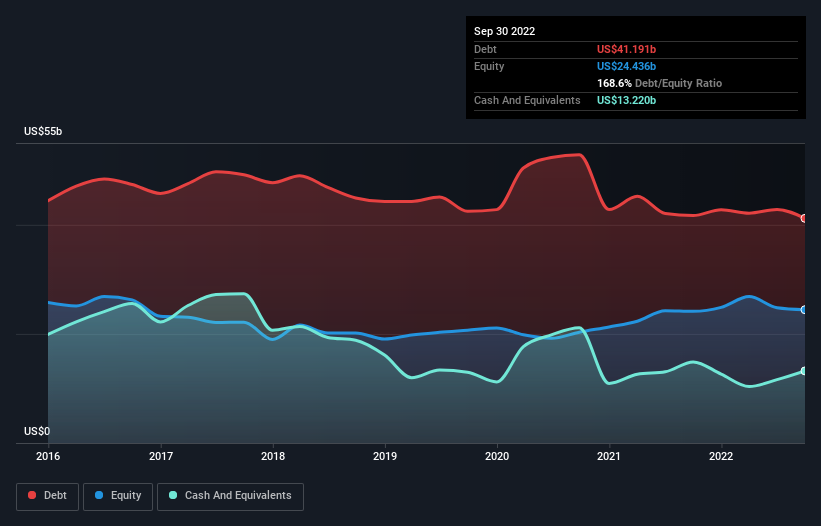

As you can see below, Coca-Cola had US$41.2b of debt, at September 2022, which is about the same as the year before. You can click the chart for greater detail. On the flip side, it has US$13.2b in cash leading to net debt of about US$28.0b.

How Strong Is Coca-Cola’s Balance Sheet?

The latest balance sheet data shows that Coca-Cola had liabilities of US$21.4b due within a year, and liabilities of US$46.6b falling due after that. On the other hand, it had cash of US$13.2b and US$3.99b worth of receivables due within a year. So it has liabilities totalling US$50.8b more than its cash and near-term receivables, combined.

Of course, Coca-Cola has a titanic market capitalization of US$271.4b, so these liabilities are probably manageable. Having said that, it’s clear that we should continue to monitor its balance sheet, lest it change for the worse.

In order to size up a company’s debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Coca-Cola’s net debt to EBITDA ratio of about 2.1 suggests only moderate use of debt. And its commanding EBIT of 44.2 times its interest expense, implies the debt load is as light as a peacock feather. Coca-Cola grew its EBIT by 3.5% in the last year. Whilst that hardly knocks our socks off it is a positive when it comes to debt. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Coca-Cola can strengthen its balance sheet over time.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Over the last three years, Coca-Cola recorded free cash flow worth a fulsome 86% of its EBIT, which is stronger than we’d usually expect. That positions it well to pay down debt if desirable to do so.

Our View

Happily, Coca-Cola’s impressive interest cover implies it has the upper hand on its debt. And that’s just the beginning of the good news since its conversion of EBIT to free cash flow is also very heartening. When we consider the range of factors above, it looks like Coca-Cola is pretty sensible with its use of debt. That means they are taking on a bit more risk, in the hope of boosting shareholder returns.