Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that ‘Volatility is far from synonymous with risk.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. Importantly, Gaia, Inc. (NASDAQ:GAIA) does carry debt. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first step when considering a company’s debt levels is to consider its cash and debt together.

What Is Gaia’s Debt?

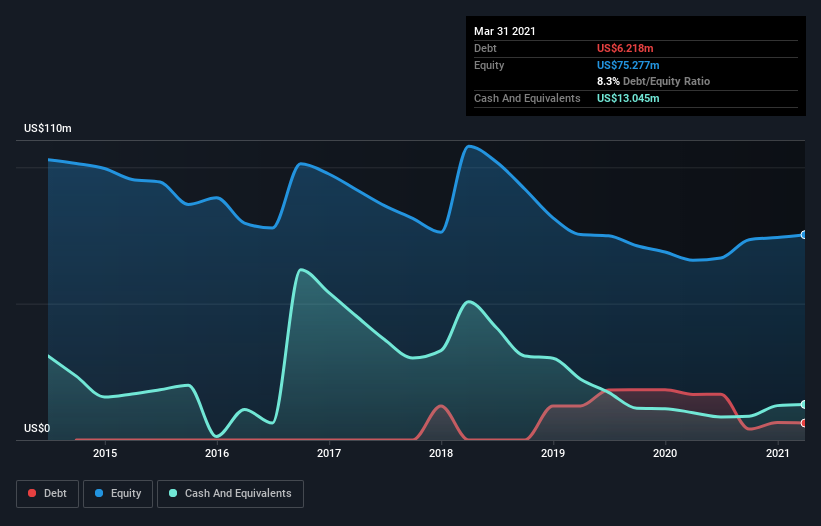

As you can see below, Gaia had US$6.22m of debt at March 2021, down from US$16.7m a year prior. But on the other hand it also has US$13.0m in cash, leading to a US$6.83m net cash position.

A Look At Gaia’s Liabilities

According to the last reported balance sheet, Gaia had liabilities of US$22.6m due within 12 months, and liabilities of US$14.3m due beyond 12 months. On the other hand, it had cash of US$13.0m and US$2.53m worth of receivables due within a year. So its liabilities total US$21.3m more than the combination of its cash and short-term receivables.

Since publicly traded Gaia shares are worth a total of US$216.8m, it seems unlikely that this level of liabilities would be a major threat. Having said that, it’s clear that we should continue to monitor its balance sheet, lest it change for the worse. While it does have liabilities worth noting, Gaia also has more cash than debt, so we’re pretty confident it can manage its debt safely. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Gaia’s ability to maintain a healthy balance sheet going forward.

Over 12 months, Gaia reported revenue of US$71m, which is a gain of 27%, although it did not report any earnings before interest and tax. With any luck the company will be able to grow its way to profitability.

So How Risky Is Gaia?

While Gaia lost money on an earnings before interest and tax (EBIT) level, it actually booked a paper profit of US$4.5m. So taking that on face value, and considering the cash, we don’t think its very risky in the near term. The good news for Gaia shareholders is that its revenue growth is strong, making it easier to raise capital if need be. But we still think it’s somewhat risky. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet.