Legendary fund manager Li Lu (who Charlie Munger backed) once said, ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. As with many other companies EchoStar Corporation (NASDAQ:SATS) makes use of debt. But the more important question is: how much risk is that debt creating?

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we examine debt levels, we first consider both cash and debt levels, together.

What Is EchoStar’s Debt?

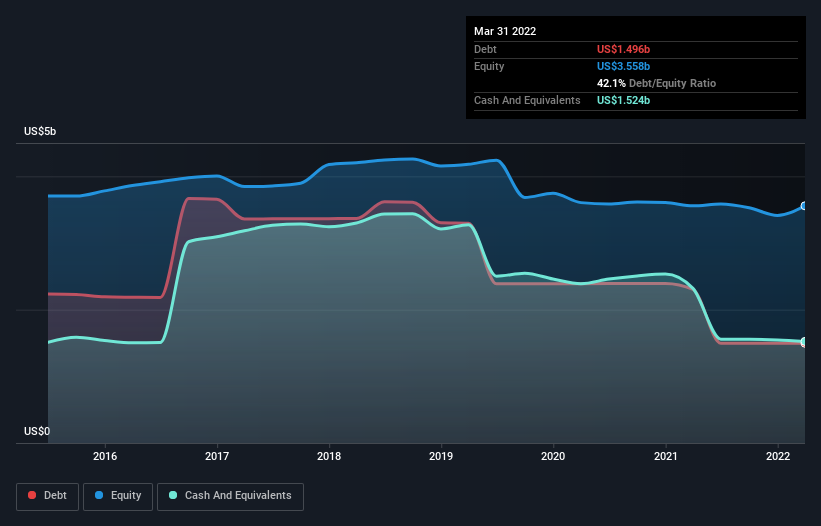

As you can see below, EchoStar had US$1.50b of debt at March 2022, down from US$2.30b a year prior. However, its balance sheet shows it holds US$1.52b in cash, so it actually has US$27.6m net cash.

A Look At EchoStar’s Liabilities

The latest balance sheet data shows that EchoStar had liabilities of US$423.7m due within a year, and liabilities of US$2.19b falling due after that. Offsetting these obligations, it had cash of US$1.52b as well as receivables valued at US$217.6m due within 12 months. So its liabilities total US$870.4m more than the combination of its cash and short-term receivables.

While this might seem like a lot, it is not so bad since EchoStar has a market capitalization of US$1.65b, and so it could probably strengthen its balance sheet by raising capital if it needed to. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk. While it does have liabilities worth noting, EchoStar also has more cash than debt, so we’re pretty confident it can manage its debt safely.

It is well worth noting that EchoStar’s EBIT shot up like bamboo after rain, gaining 33% in the last twelve months. That’ll make it easier to manage its debt. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if EchoStar can strengthen its balance sheet over time.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. EchoStar may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. Over the most recent three years, EchoStar recorded free cash flow worth 77% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Summing up

While EchoStar does have more liabilities than liquid assets, it also has net cash of US$27.6m. And it impressed us with its EBIT growth of 33% over the last year. So we don’t have any problem with EchoStar’s use of debt. There’s no doubt that we learn most about debt from the balance sheet.