The external fund manager backed by Berkshire Hathaway’s Charlie Munger, Li Lu, makes no bones about it when he says ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We note that Adobe Inc. (NASDAQ:ADBE) does have debt on its balance sheet. But the more important question is: how much risk is that debt creating?

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we examine debt levels, we first consider both cash and debt levels, together.

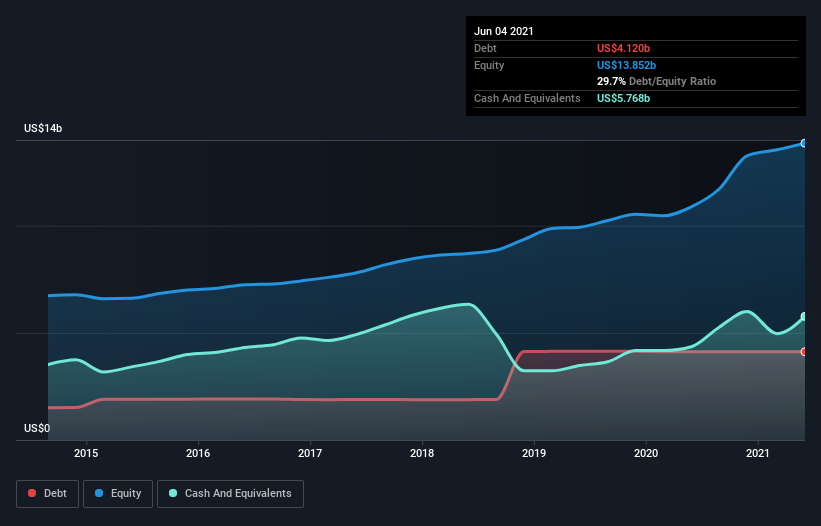

What Is Adobe’s Net Debt?

The chart below, which you can click on for greater detail, shows that Adobe had US$4.12b in debt in June 2021; about the same as the year before. However, its balance sheet shows it holds US$5.77b in cash, so it actually has US$1.65b net cash.

How Healthy Is Adobe’s Balance Sheet?

According to the last reported balance sheet, Adobe had liabilities of US$6.15b due within 12 months, and liabilities of US$5.59b due beyond 12 months. Offsetting this, it had US$5.77b in cash and US$1.48b in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$4.49b.

This state of affairs indicates that Adobe’s balance sheet looks quite solid, as its total liabilities are just about equal to its liquid assets. So while it’s hard to imagine that the US$271.1b company is struggling for cash, we still think it’s worth monitoring its balance sheet. Despite its noteworthy liabilities, Adobe boasts net cash, so it’s fair to say it does not have a heavy debt load!

In addition to that, we’re happy to report that Adobe has boosted its EBIT by 36%, thus reducing the spectre of future debt repayments. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Adobe can strengthen its balance sheet over time.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. Adobe may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. Over the last three years, Adobe actually produced more free cash flow than EBIT. That sort of strong cash generation warms our hearts like a puppy in a bumblebee suit.

Summing up

While it is always sensible to look at a company’s total liabilities, it is very reassuring that Adobe has US$1.65b in net cash. The cherry on top was that in converted 126% of that EBIT to free cash flow, bringing in US$6.6b. So is Adobe’s debt a risk? It doesn’t seem so to us. There’s no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet.