Legendary fund manager Li Lu (who Charlie Munger backed) once said, ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We note that CRH Medical Corporation (TSE:CRH) does have debt on its balance sheet. But should shareholders be worried about its use of debt?

When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we think about a company’s use of debt, we first look at cash and debt together.

How Much Debt Does CRH Medical Carry?

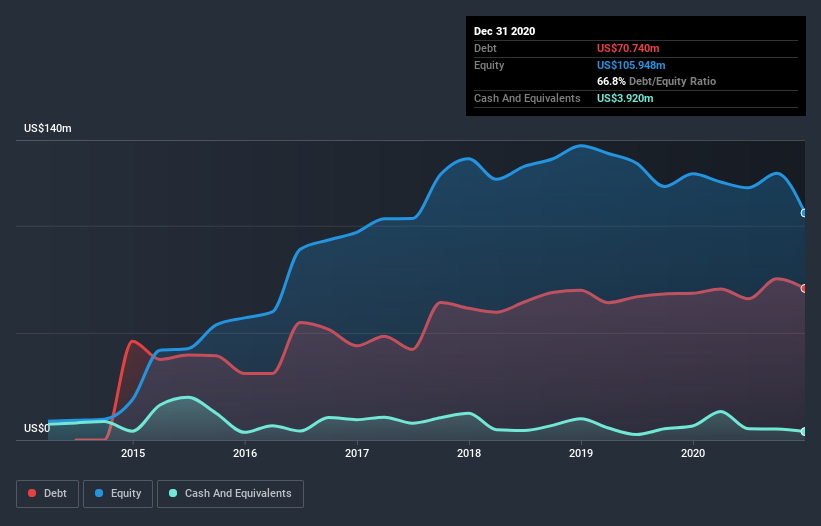

As you can see below, CRH Medical had US$70.7m of debt, at December 2020, which is about the same as the year before. You can click the chart for greater detail. However, because it has a cash reserve of US$3.92m, its net debt is less, at about US$66.8m.

A Look At CRH Medical’s Liabilities

According to the last reported balance sheet, CRH Medical had liabilities of US$11.8m due within 12 months, and liabilities of US$74.1m due beyond 12 months. Offsetting these obligations, it had cash of US$3.92m as well as receivables valued at US$26.5m due within 12 months. So its liabilities total US$55.4m more than the combination of its cash and short-term receivables.

Given CRH Medical has a market capitalization of US$282.3m, it’s hard to believe these liabilities pose much threat. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward. There’s no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine CRH Medical’s ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Over 12 months, CRH Medical made a loss at the EBIT level, and saw its revenue drop to US$106m, which is a fall of 12%. We would much prefer see growth.

Caveat Emptor

While CRH Medical’s falling revenue is about as heartwarming as a wet blanket, arguably its earnings before interest and tax (EBIT) loss is even less appealing. Indeed, it lost US$6.5m at the EBIT level. When we look at that and recall the liabilities on its balance sheet, relative to cash, it seems unwise to us for the company to have any debt. Quite frankly we think the balance sheet is far from match-fit, although it could be improved with time. For example, we would not want to see a repeat of last year’s loss of US$24m. So in short it’s a really risky stock. The balance sheet is clearly the area to focus on when you are analysing debt.