Howard Marks put it nicely when he said that, rather than worrying about share price volatility, ‘The possibility of permanent loss is the risk I worry about… and every practical investor I know worries about.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. As with many other companies Comcast Corporation (NASDAQ:CMCS.A) makes use of debt. But should shareholders be worried about its use of debt?

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. When we examine debt levels, we first consider both cash and debt levels, together.

What Is Comcast’s Net Debt?

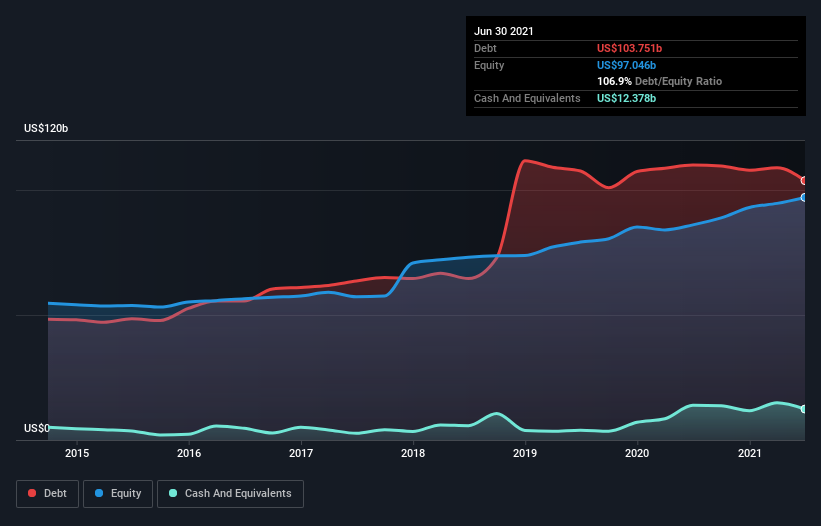

The image below, which you can click on for greater detail, shows that Comcast had debt of US$103.8b at the end of June 2021, a reduction from US$110.0b over a year. However, because it has a cash reserve of US$12.4b, its net debt is less, at about US$91.4b.

A Look At Comcast’s Liabilities

Zooming in on the latest balance sheet data, we can see that Comcast had liabilities of US$29.3b due within 12 months and liabilities of US$150.6b due beyond that. On the other hand, it had cash of US$12.4b and US$11.1b worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$156.5b.

This deficit isn’t so bad because Comcast is worth a massive US$262.9b, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. However, it is still worthwhile taking a close look at its ability to pay off debt.

In order to size up a company’s debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Comcast’s debt is 2.9 times its EBITDA, and its EBIT cover its interest expense 4.2 times over. This suggests that while the debt levels are significant, we’d stop short of calling them problematic. More concerning, Comcast saw its EBIT drop by 7.7% in the last twelve months. If that earnings trend continues the company will face an uphill battle to pay off its debt. There’s no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Comcast’s ability to maintain a healthy balance sheet going forward.

Finally, a business needs free cash flow to pay off debt; accounting profits just don’t cut it. So we always check how much of that EBIT is translated into free cash flow. During the last three years, Comcast produced sturdy free cash flow equating to 64% of its EBIT, about what we’d expect. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Our View

Neither Comcast’s ability to grow its EBIT nor its level of total liabilities gave us confidence in its ability to take on more debt. But it seems to be able to convert EBIT to free cash flow without much trouble. When we consider all the factors discussed, it seems to us that Comcast is taking some risks with its use of debt. So while that leverage does boost returns on equity, we wouldn’t really want to see it increase from here.