Howard Marks put it nicely when he said that, rather than worrying about share price volatility, ‘The possibility of permanent loss is the risk I worry about… and every practical investor I know worries about.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. As with many other companies Tandem Diabetes Care, Inc. (NASDAQ:TNDM) makes use of debt. But should shareholders be worried about its use of debt?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

What Is Tandem Diabetes Care’s Net Debt?

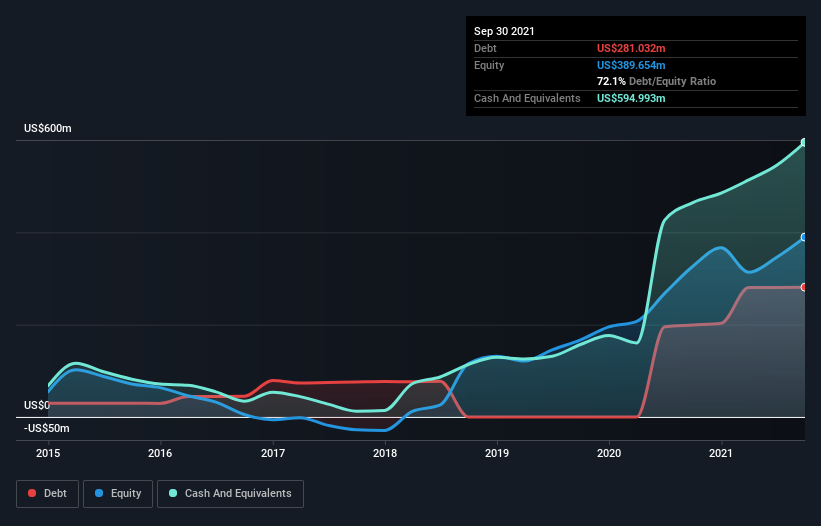

The image below, which you can click on for greater detail, shows that at September 2021 Tandem Diabetes Care had debt of US$281.0m, up from US$199.1m in one year. But on the other hand it also has US$595.0m in cash, leading to a US$314.0m net cash position.

How Healthy Is Tandem Diabetes Care’s Balance Sheet?

According to the last reported balance sheet, Tandem Diabetes Care had liabilities of US$119.7m due within 12 months, and liabilities of US$341.0m due beyond 12 months. Offsetting these obligations, it had cash of US$595.0m as well as receivables valued at US$87.5m due within 12 months. So it actually has US$221.8m more liquid assets than total liabilities.

This surplus suggests that Tandem Diabetes Care has a conservative balance sheet, and could probably eliminate its debt without much difficulty. Simply put, the fact that Tandem Diabetes Care has more cash than debt is arguably a good indication that it can manage its debt safely.

We also note that Tandem Diabetes Care improved its EBIT from a last year’s loss to a positive US$29m. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Tandem Diabetes Care can strengthen its balance sheet over time.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. Tandem Diabetes Care may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. Over the last year, Tandem Diabetes Care actually produced more free cash flow than EBIT. That sort of strong cash generation warms our hearts like a puppy in a bumblebee suit.

Summing up

While we empathize with investors who find debt concerning, you should keep in mind that Tandem Diabetes Care has net cash of US$314.0m, as well as more liquid assets than liabilities. And it impressed us with free cash flow of US$85m, being 298% of its EBIT. So we don’t think Tandem Diabetes Care’s use of debt is risky.