Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that ‘Volatility is far from synonymous with risk.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. As with many other companies Select Medical Holdings Corporation (NYSE:SEM) makes use of debt. But the more important question is: how much risk is that debt creating?

When Is Debt Dangerous?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

What Is Select Medical Holdings’s Net Debt?

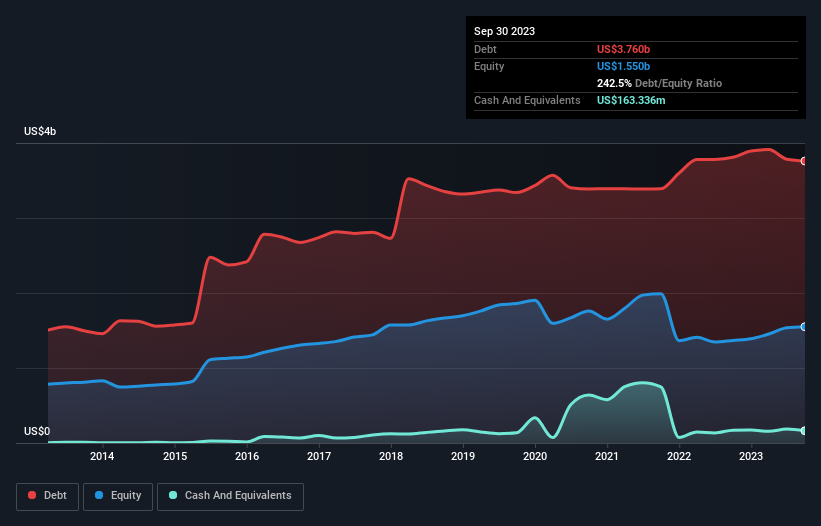

As you can see below, Select Medical Holdings had US$3.76b of debt, at September 2023, which is about the same as the year before. You can click the chart for greater detail. However, it does have US$163.3m in cash offsetting this, leading to net debt of about US$3.60b.

How Strong Is Select Medical Holdings’ Balance Sheet?

We can see from the most recent balance sheet that Select Medical Holdings had liabilities of US$1.17b falling due within a year, and liabilities of US$4.97b due beyond that. Offsetting this, it had US$163.3m in cash and US$944.2m in receivables that were due within 12 months. So it has liabilities totalling US$5.03b more than its cash and near-term receivables, combined.

Given this deficit is actually higher than the company’s market capitalization of US$3.39b, we think shareholders really should watch Select Medical Holdings’s debt levels, like a parent watching their child ride a bike for the first time. In the scenario where the company had to clean up its balance sheet quickly, it seems likely shareholders would suffer extensive dilution.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Select Medical Holdings has a debt to EBITDA ratio of 4.9 and its EBIT covered its interest expense 2.7 times. This suggests that while the debt levels are significant, we’d stop short of calling them problematic. Looking on the bright side, Select Medical Holdings boosted its EBIT by a silky 45% in the last year. Like the milk of human kindness that sort of growth increases resilience, making the company more capable of managing debt. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Select Medical Holdings can strengthen its balance sheet over time.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. In the last three years, Select Medical Holdings’s free cash flow amounted to 47% of its EBIT, less than we’d expect. That weak cash conversion makes it more difficult to handle indebtedness.

Our View

On the face of it, Select Medical Holdings’s net debt to EBITDA left us tentative about the stock, and its level of total liabilities was no more enticing than the one empty restaurant on the busiest night of the year. But at least it’s pretty decent at growing its EBIT; that’s encouraging. We should also note that Healthcare industry companies like Select Medical Holdings commonly do use debt without problems. Once we consider all the factors above, together, it seems to us that Select Medical Holdings’s debt is making it a bit risky. Some people like that sort of risk, but we’re mindful of the potential pitfalls, so we’d probably prefer it carry less debt.