The external fund manager backed by Berkshire Hathaway’s Charlie Munger, Li Lu, makes no bones about it when he says ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. Importantly, Medtronic plc (NYSE:MDT) does carry debt. But the more important question is: how much risk is that debt creating?

When Is Debt A Problem?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first step when considering a company’s debt levels is to consider its cash and debt together.

What Is Medtronic’s Debt?

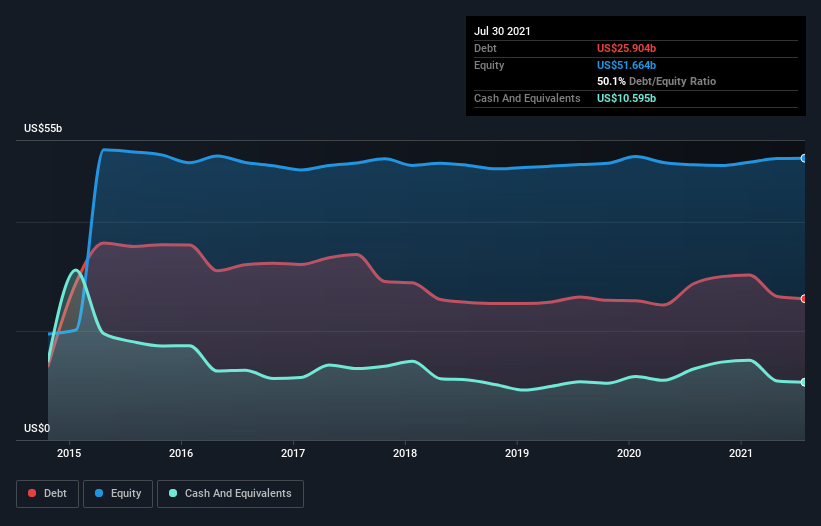

The image below, which you can click on for greater detail, shows that Medtronic had debt of US$25.9b at the end of July 2021, a reduction from US$28.6b over a year. However, it does have US$10.6b in cash offsetting this, leading to net debt of about US$15.3b.

A Look At Medtronic’s Liabilities

We can see from the most recent balance sheet that Medtronic had liabilities of US$7.76b falling due within a year, and liabilities of US$32.4b due beyond that. Offsetting this, it had US$10.6b in cash and US$5.43b in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$24.1b.

Since publicly traded Medtronic shares are worth a very impressive total of US$176.5b, it seems unlikely that this level of liabilities would be a major threat. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Medtronic’s net debt of 1.7 times EBITDA suggests graceful use of debt. And the alluring interest cover (EBIT of 9.1 times interest expense) certainly does not do anything to dispel this impression. In addition to that, we’re happy to report that Medtronic has boosted its EBIT by 49%, thus reducing the spectre of future debt repayments. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Medtronic’s ability to maintain a healthy balance sheet going forward. So if you’re focused on the future you can check out this free report showing analyst profit forecasts.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. During the last three years, Medtronic generated free cash flow amounting to a very robust 92% of its EBIT, more than we’d expect. That positions it well to pay down debt if desirable to do so.

Our View

Medtronic’s conversion of EBIT to free cash flow suggests it can handle its debt as easily as Cristiano Ronaldo could score a goal against an under 14’s goalkeeper. And the good news does not stop there, as its EBIT growth rate also supports that impression! We would also note that Medical Equipment industry companies like Medtronic commonly do use debt without problems. Considering this range of factors, it seems to us that Medtronic is quite prudent with its debt, and the risks seem well managed. So we’re not worried about the use of a little leverage on the balance sheet. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet.