Legendary fund manager Li Lu (who Charlie Munger backed) once said, ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We can see that NOV Inc. (NYSE:NOV) does use debt in its business. But the more important question is: how much risk is that debt creating?

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

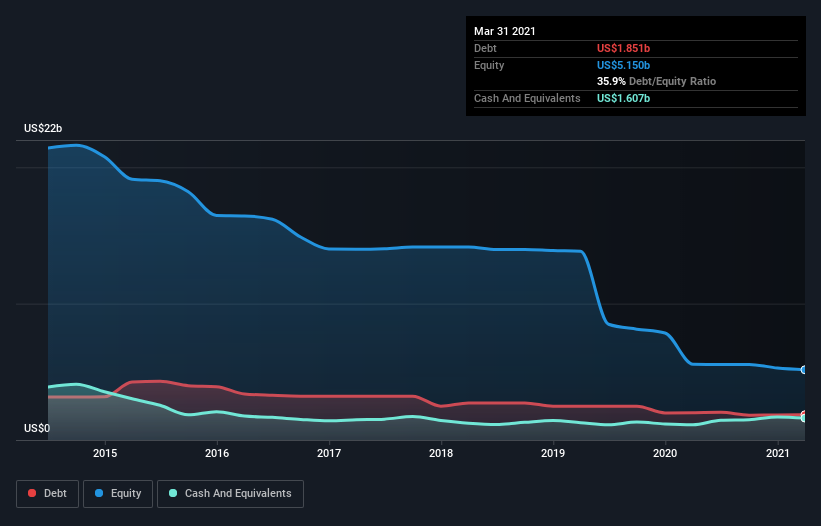

How Much Debt Does NOV Carry?

As you can see below, NOV had US$1.85b of debt at March 2021, down from US$2.00b a year prior. However, because it has a cash reserve of US$1.61b, its net debt is less, at about US$244.0m.

How Strong Is NOV’s Balance Sheet?

Zooming in on the latest balance sheet data, we can see that NOV had liabilities of US$1.93b due within 12 months and liabilities of US$2.59b due beyond that. Offsetting these obligations, it had cash of US$1.61b as well as receivables valued at US$1.84b due within 12 months. So it has liabilities totalling US$1.07b more than its cash and near-term receivables, combined.

Since publicly traded NOV shares are worth a total of US$6.81b, it seems unlikely that this level of liabilities would be a major threat. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine NOV’s ability to maintain a healthy balance sheet going forward.

In the last year NOV had a loss before interest and tax, and actually shrunk its revenue by 35%, to US$5.5b. That makes us nervous, to say the least.

Caveat Emptor

Not only did NOV’s revenue slip over the last twelve months, but it also produced negative earnings before interest and tax (EBIT). To be specific the EBIT loss came in at US$563m. When we look at that and recall the liabilities on its balance sheet, relative to cash, it seems unwise to us for the company to have any debt. So we think its balance sheet is a little strained, though not beyond repair. We would feel better if it turned its trailing twelve month loss of US$610m into a profit. In the meantime, we consider the stock very risky. There’s no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet.