David Iben put it well when he said, ‘Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. Importantly, Ceridian HCM Holding Inc. (NYSE:CDAY) does carry debt. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we examine debt levels, we first consider both cash and debt levels, together.

What Is Ceridian HCM Holding’s Net Debt?

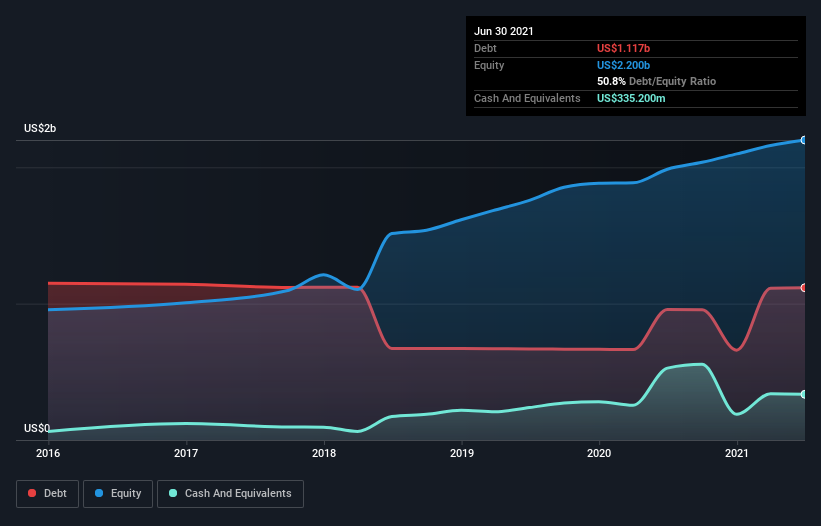

You can click the graphic below for the historical numbers, but it shows that as of June 2021 Ceridian HCM Holding had US$1.12b of debt, an increase on US$956.8m, over one year. However, it also had US$335.2m in cash, and so its net debt is US$781.4m.

How Strong Is Ceridian HCM Holding’s Balance Sheet?

The latest balance sheet data shows that Ceridian HCM Holding had liabilities of US$3.37b due within a year, and liabilities of US$1.23b falling due after that. On the other hand, it had cash of US$335.2m and US$118.2m worth of receivables due within a year. So its liabilities total US$4.15b more than the combination of its cash and short-term receivables.

This deficit isn’t so bad because Ceridian HCM Holding is worth a massive US$17.2b, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. But it’s clear that we should definitely closely examine whether it can manage its debt without dilution. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Ceridian HCM Holding’s ability to maintain a healthy balance sheet going forward.

Over 12 months, Ceridian HCM Holding reported revenue of US$912m, which is a gain of 8.7%, although it did not report any earnings before interest and tax. That rate of growth is a bit slow for our taste, but it takes all types to make a world.

Caveat Emptor

Importantly, Ceridian HCM Holding had an earnings before interest and tax (EBIT) loss over the last year. To be specific the EBIT loss came in at US$7.4m. When we look at that and recall the liabilities on its balance sheet, relative to cash, it seems unwise to us for the company to have any debt. So we think its balance sheet is a little strained, though not beyond repair. Another cause for caution is that is bled US$92m in negative free cash flow over the last twelve months. So to be blunt we think it is risky.