Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that ‘Volatility is far from synonymous with risk.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. As with many other companies Cyren Ltd. (NASDAQ:CYRN) makes use of debt. But the more important question is: how much risk is that debt creating?

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

How Much Debt Does Cyren Carry?

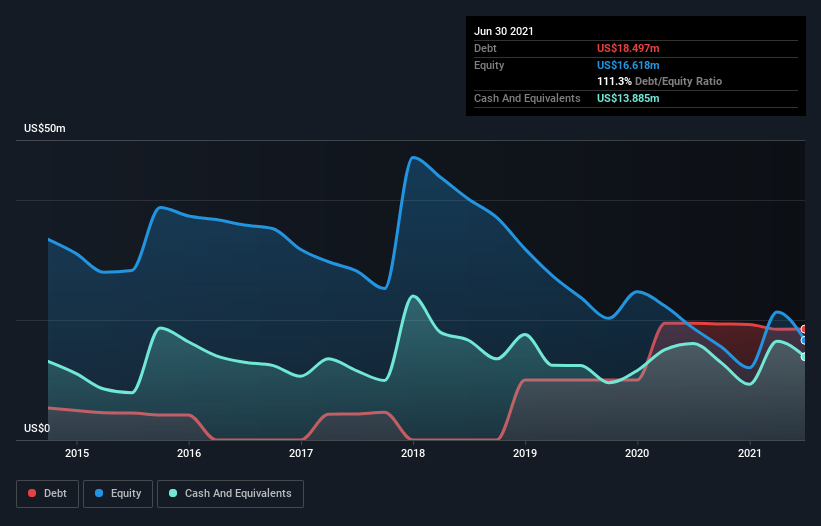

The image below, which you can click on for greater detail, shows that Cyren had debt of US$18.5m at the end of June 2021, a reduction from US$19.4m over a year. However, it also had US$13.9m in cash, and so its net debt is US$4.61m.

How Healthy Is Cyren’s Balance Sheet?

We can see from the most recent balance sheet that Cyren had liabilities of US$24.7m falling due within a year, and liabilities of US$19.8m due beyond that. Offsetting this, it had US$13.9m in cash and US$1.41m in receivables that were due within 12 months. So it has liabilities totalling US$29.3m more than its cash and near-term receivables, combined.

This deficit is considerable relative to its market capitalization of US$41.2m, so it does suggest shareholders should keep an eye on Cyren’s use of debt. This suggests shareholders would be heavily diluted if the company needed to shore up its balance sheet in a hurry. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Cyren’s ability to maintain a healthy balance sheet going forward.

In the last year Cyren had a loss before interest and tax, and actually shrunk its revenue by 10%, to US$34m. We would much prefer see growth.

Caveat Emptor

While Cyren’s falling revenue is about as heartwarming as a wet blanket, arguably its earnings before interest and tax (EBIT) loss is even less appealing. Its EBIT loss was a whopping US$18m. When we look at that and recall the liabilities on its balance sheet, relative to cash, it seems unwise to us for the company to have any debt. Quite frankly we think the balance sheet is far from match-fit, although it could be improved with time. Another cause for caution is that is bled US$15m in negative free cash flow over the last twelve months. So in short it’s a really risky stock. The balance sheet is clearly the area to focus on when you are analysing debt.