The external fund manager backed by Berkshire Hathaway’s Charlie Munger, Li Lu, makes no bones about it when he says ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We can see that Centennial Resource Development, Inc. (NASDAQ:CDEV) does use debt in its business. But the more important question is: how much risk is that debt creating?

When Is Debt Dangerous?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first step when considering a company’s debt levels is to consider its cash and debt together.

What Is Centennial Resource Development’s Debt?

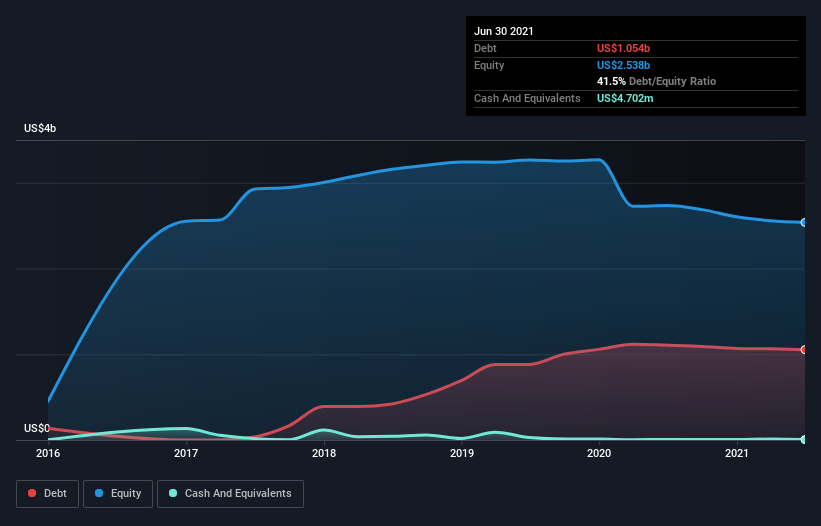

The image below, which you can click on for greater detail, shows that Centennial Resource Development had debt of US$1.05b at the end of June 2021, a reduction from US$1.11b over a year. Net debt is about the same, since the it doesn’t have much cash.

How Strong Is Centennial Resource Development’s Balance Sheet?

The latest balance sheet data shows that Centennial Resource Development had liabilities of US$220.9m due within a year, and liabilities of US$1.12b falling due after that. Offsetting these obligations, it had cash of US$4.70m as well as receivables valued at US$89.6m due within 12 months. So it has liabilities totalling US$1.24b more than its cash and near-term receivables, combined.

This deficit is considerable relative to its market capitalization of US$1.45b, so it does suggest shareholders should keep an eye on Centennial Resource Development’s use of debt. Should its lenders demand that it shore up the balance sheet, shareholders would likely face severe dilution. There’s no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Centennial Resource Development’s ability to maintain a healthy balance sheet going forward.

Over 12 months, Centennial Resource Development made a loss at the EBIT level, and saw its revenue drop to US$722m, which is a fall of 6.1%. That’s not what we would hope to see.

Caveat Emptor

Over the last twelve months Centennial Resource Development produced an earnings before interest and tax (EBIT) loss. Indeed, it lost US$116m at the EBIT level. Considering that alongside the liabilities mentioned above does not give us much confidence that company should be using so much debt. Quite frankly we think the balance sheet is far from match-fit, although it could be improved with time. We would feel better if it turned its trailing twelve month loss of US$200m into a profit. In the meantime, we consider the stock very risky. When analysing debt levels, the balance sheet is the obvious place to start.