Howard Marks put it nicely when he said that, rather than worrying about share price volatility, ‘The possibility of permanent loss is the risk I worry about… and every practical investor I know worries about.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. As with many other companies Waters Corporation (NYSE:WAT) makes use of debt. But the more important question is: how much risk is that debt creating?

When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

What Is Waters’s Debt?

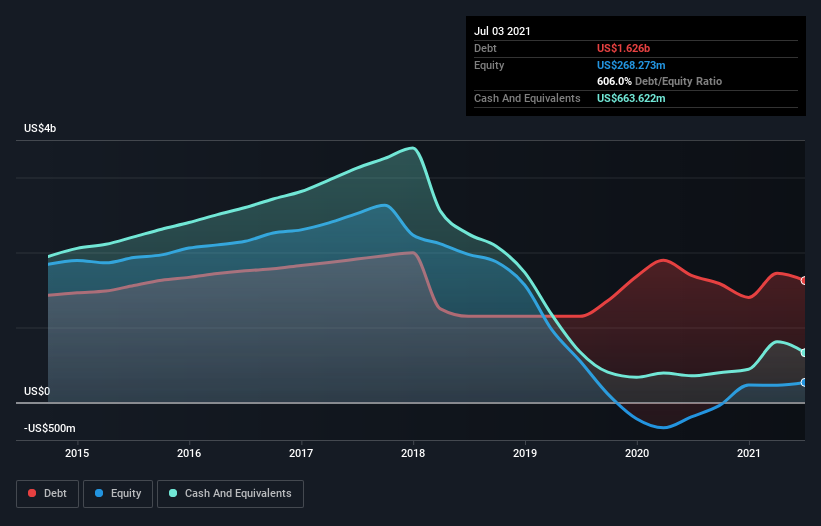

As you can see below, Waters had US$1.63b of debt at July 2021, down from US$1.70b a year prior. However, it does have US$663.6m in cash offsetting this, leading to net debt of about US$962.2m.

A Look At Waters’ Liabilities

The latest balance sheet data shows that Waters had liabilities of US$681.0m due within a year, and liabilities of US$2.15b falling due after that. Offsetting this, it had US$663.6m in cash and US$543.1m in receivables that were due within 12 months. So its liabilities total US$1.63b more than the combination of its cash and short-term receivables.

Of course, Waters has a titanic market capitalization of US$24.5b, so these liabilities are probably manageable. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Waters’s net debt is only 1.0 times its EBITDA. And its EBIT covers its interest expense a whopping 28.5 times over. So you could argue it is no more threatened by its debt than an elephant is by a mouse. Also positive, Waters grew its EBIT by 28% in the last year, and that should make it easier to pay down debt, going forward. There’s no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Waters can strengthen its balance sheet over time.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So we always check how much of that EBIT is translated into free cash flow. During the last three years, Waters produced sturdy free cash flow equating to 76% of its EBIT, about what we’d expect. This cold hard cash means it can reduce its debt when it wants to.

Our View

Waters’s interest cover suggests it can handle its debt as easily as Cristiano Ronaldo could score a goal against an under 14’s goalkeeper. And the good news does not stop there, as its EBIT growth rate also supports that impression! Considering this range of factors, it seems to us that Waters is quite prudent with its debt, and the risks seem well managed. So we’re not worried about the use of a little leverage on the balance sheet.