Howard Marks put it nicely when he said that, rather than worrying about share price volatility, ‘The possibility of permanent loss is the risk I worry about… and every practical investor I know worries about.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. We can see that Chevron Corporation (NYSE:CVX) does use debt in its business. But is this debt a concern to shareholders?

What Risk Does Debt Bring?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we think about a company’s use of debt, we first look at cash and debt together.

What Is Chevron’s Debt?

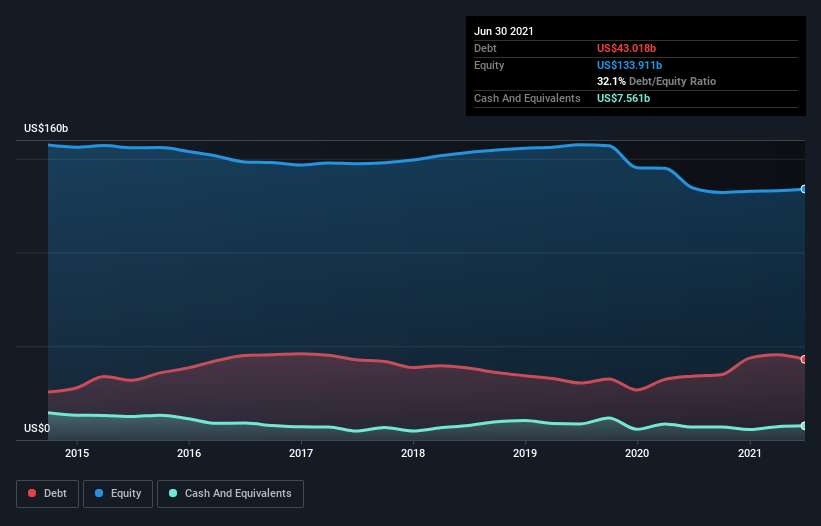

As you can see below, at the end of June 2021, Chevron had US$43.0b of debt, up from US$34.1b a year ago. Click the image for more detail. However, it also had US$7.56b in cash, and so its net debt is US$35.5b.

A Look At Chevron’s Liabilities

We can see from the most recent balance sheet that Chevron had liabilities of US$28.1b falling due within a year, and liabilities of US$80.7b due beyond that. Offsetting this, it had US$7.56b in cash and US$15.6b in receivables that were due within 12 months. So its liabilities total US$85.7b more than the combination of its cash and short-term receivables.

This deficit isn’t so bad because Chevron is worth a massive US$188.2b, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. However, it is still worthwhile taking a close look at its ability to pay off debt.

In order to size up a company’s debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

With a debt to EBITDA ratio of 1.6, Chevron uses debt artfully but responsibly. And the alluring interest cover (EBIT of 9.0 times interest expense) certainly does not do anything to dispel this impression. It was also good to see that despite losing money on the EBIT line last year, Chevron turned things around in the last 12 months, delivering and EBIT of US$6.7b. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Chevron can strengthen its balance sheet over time.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So it’s worth checking how much of the earnings before interest and tax (EBIT) is backed by free cash flow. Happily for any shareholders, Chevron actually produced more free cash flow than EBIT over the last year. There’s nothing better than incoming cash when it comes to staying in your lenders’ good graces.

Our View

The good news is that Chevron’s demonstrated ability to convert EBIT to free cash flow delights us like a fluffy puppy does a toddler. But, on a more sombre note, we are a little concerned by its level of total liabilities. Looking at all the aforementioned factors together, it strikes us that Chevron can handle its debt fairly comfortably. Of course, while this leverage can enhance returns on equity, it does bring more risk, so it’s worth keeping an eye on this one. The balance sheet is clearly the area to focus on when you are analysing debt.