Legendary fund manager Li Lu (who Charlie Munger backed) once said, ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. As with many other companies Methode Electronics, Inc. (NYSE:MEI) makes use of debt. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first step when considering a company’s debt levels is to consider its cash and debt together.

What Is Methode Electronics’s Net Debt?

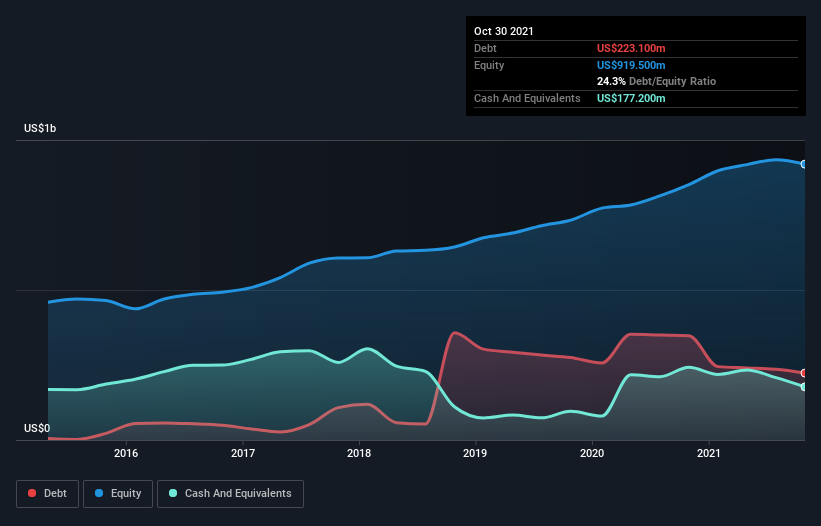

As you can see below, Methode Electronics had US$223.1m of debt at October 2021, down from US$244.6m a year prior. On the flip side, it has US$177.2m in cash leading to net debt of about US$45.9m.

How Healthy Is Methode Electronics’ Balance Sheet?

We can see from the most recent balance sheet that Methode Electronics had liabilities of US$207.8m falling due within a year, and liabilities of US$303.4m due beyond that. On the other hand, it had cash of US$177.2m and US$295.0m worth of receivables due within a year. So it has liabilities totalling US$39.0m more than its cash and near-term receivables, combined.

Given Methode Electronics has a market capitalization of US$1.61b, it’s hard to believe these liabilities pose much threat. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time.

In order to size up a company’s debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Methode Electronics has a low net debt to EBITDA ratio of only 0.24. And its EBIT covers its interest expense a whopping 31.9 times over. So we’re pretty relaxed about its super-conservative use of debt. On the other hand, Methode Electronics saw its EBIT drop by 8.1% in the last twelve months. If earnings continue to decline at that rate the company may have increasing difficulty managing its debt load. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Methode Electronics’s ability to maintain a healthy balance sheet going forward.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So it’s worth checking how much of that EBIT is backed by free cash flow. During the last three years, Methode Electronics generated free cash flow amounting to a very robust 85% of its EBIT, more than we’d expect. That puts it in a very strong position to pay down debt.

Our View

Methode Electronics’s interest cover suggests it can handle its debt as easily as Cristiano Ronaldo could score a goal against an under 14’s goalkeeper. But, on a more sombre note, we are a little concerned by its EBIT growth rate. Looking at the bigger picture, we think Methode Electronics’s use of debt seems quite reasonable and we’re not concerned about it. After all, sensible leverage can boost returns on equity. There’s no doubt that we learn most about debt from the balance sheet.