Warren Buffett famously said, ‘Volatility is far from synonymous with risk.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. Importantly, Micron Technology, Inc. (NASDAQ:MU) does carry debt. But should shareholders be worried about its use of debt?

What Risk Does Debt Bring?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first step when considering a company’s debt levels is to consider its cash and debt together.

How Much Debt Does Micron Technology Carry?

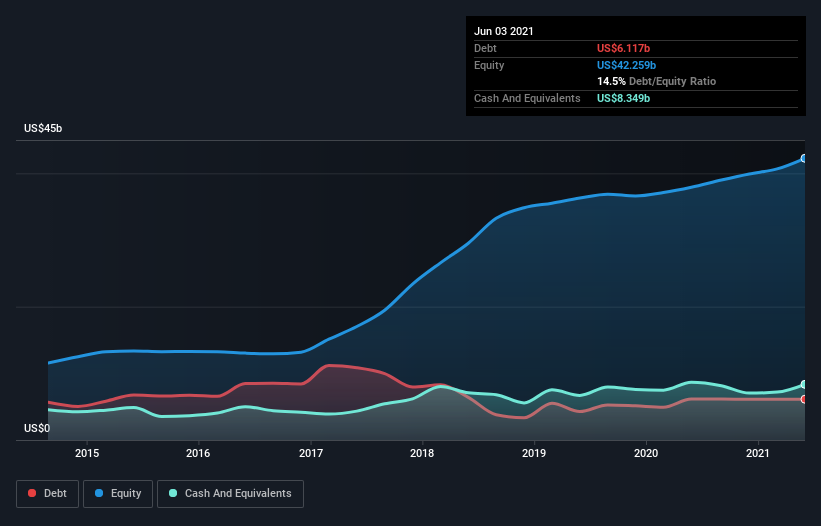

As you can see below, Micron Technology had US$6.12b of debt, at June 2021, which is about the same as the year before. You can click the chart for greater detail. But it also has US$8.35b in cash to offset that, meaning it has US$2.23b net cash.

How Strong Is Micron Technology’s Balance Sheet?

According to the last reported balance sheet, Micron Technology had liabilities of US$5.46b due within 12 months, and liabilities of US$8.22b due beyond 12 months. Offsetting this, it had US$8.35b in cash and US$4.23b in receivables that were due within 12 months. So its liabilities total US$1.10b more than the combination of its cash and short-term receivables.

This state of affairs indicates that Micron Technology’s balance sheet looks quite solid, as its total liabilities are just about equal to its liquid assets. So it’s very unlikely that the US$90.4b company is short on cash, but still worth keeping an eye on the balance sheet. Despite its noteworthy liabilities, Micron Technology boasts net cash, so it’s fair to say it does not have a heavy debt load!

Even more impressive was the fact that Micron Technology grew its EBIT by 103% over twelve months. That boost will make it even easier to pay down debt going forward. There’s no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Micron Technology can strengthen its balance sheet over time.

Finally, a business needs free cash flow to pay off debt; accounting profits just don’t cut it. While Micron Technology has net cash on its balance sheet, it’s still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. In the last three years, Micron Technology’s free cash flow amounted to 37% of its EBIT, less than we’d expect. That weak cash conversion makes it more difficult to handle indebtedness.

Summing up

While it is always sensible to look at a company’s total liabilities, it is very reassuring that Micron Technology has US$2.23b in net cash. And it impressed us with its EBIT growth of 103% over the last year. So we don’t think Micron Technology’s use of debt is risky. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet.