David Iben put it well when he said, ‘Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that Fabrinet (NYSE:FN) does use debt in its business. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

What Is Fabrinet’s Net Debt?

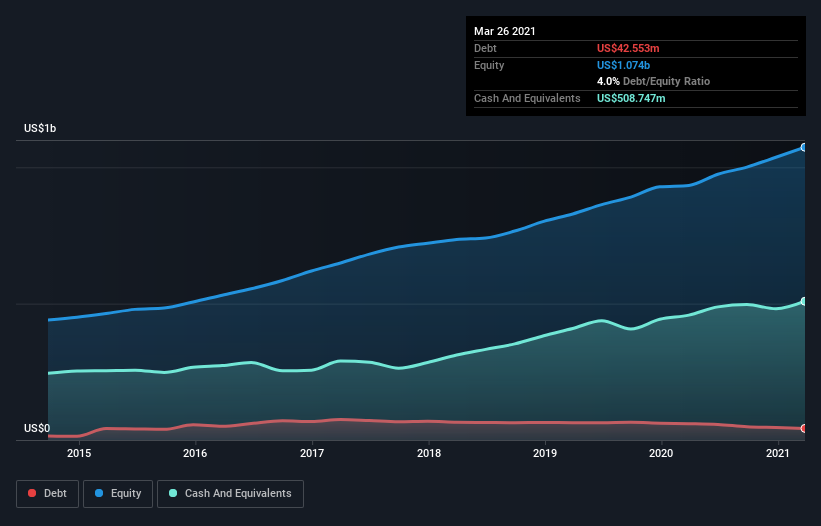

The image below, which you can click on for greater detail, shows that Fabrinet had debt of US$42.6m at the end of March 2021, a reduction from US$59.9m over a year. However, it does have US$508.7m in cash offsetting this, leading to net cash of US$466.2m.

NYSE:FN Debt to Equity History July 5th 2021

How Healthy Is Fabrinet’s Balance Sheet?

We can see from the most recent balance sheet that Fabrinet had liabilities of US$366.2m falling due within a year, and liabilities of US$62.1m due beyond that. Offsetting these obligations, it had cash of US$508.7m as well as receivables valued at US$350.5m due within 12 months. So it actually has US$430.9m more liquid assets than total liabilities.

This short term liquidity is a sign that Fabrinet could probably pay off its debt with ease, as its balance sheet is far from stretched. Succinctly put, Fabrinet boasts net cash, so it’s fair to say it does not have a heavy debt load!

Also good is that Fabrinet grew its EBIT at 14% over the last year, further increasing its ability to manage debt. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Fabrinet can strengthen its balance sheet over time.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. While Fabrinet has net cash on its balance sheet, it’s still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. Over the last three years, Fabrinet recorded free cash flow worth a fulsome 86% of its EBIT, which is stronger than we’d usually expect. That positions it well to pay down debt if desirable to do so.

Summing up

While we empathize with investors who find debt concerning, you should keep in mind that Fabrinet has net cash of US$466.2m, as well as more liquid assets than liabilities. The cherry on top was that in converted 86% of that EBIT to free cash flow, bringing in US$75m. So we don’t think Fabrinet’s use of debt is risky.