Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that ‘Volatility is far from synonymous with risk.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, Key Tronic Corporation (NASDAQ:KTCC) does carry debt. But the more important question is: how much risk is that debt creating?

When Is Debt A Problem?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. When we examine debt levels, we first consider both cash and debt levels, together.

How Much Debt Does Key Tronic Carry?

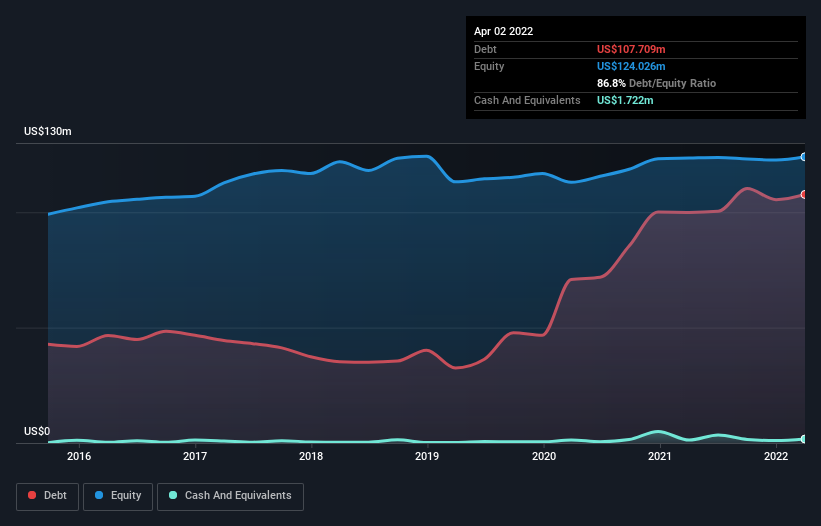

The image below, which you can click on for greater detail, shows that at April 2022 Key Tronic had debt of US$107.7m, up from US$99.9m in one year. And it doesn’t have much cash, so its net debt is about the same.

How Healthy Is Key Tronic’s Balance Sheet?

The latest balance sheet data shows that Key Tronic had liabilities of US$164.3m due within a year, and liabilities of US$123.1m falling due after that. On the other hand, it had cash of US$1.72m and US$161.3m worth of receivables due within a year. So its liabilities total US$124.4m more than the combination of its cash and short-term receivables.

This deficit casts a shadow over the US$54.9m company, like a colossus towering over mere mortals. So we’d watch its balance sheet closely, without a doubt. At the end of the day, Key Tronic would probably need a major re-capitalization if its creditors were to demand repayment.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Weak interest cover of 1.7 times and a disturbingly high net debt to EBITDA ratio of 7.7 hit our confidence in Key Tronic like a one-two punch to the gut. This means we’d consider it to have a heavy debt load. Another concern for investors might be that Key Tronic’s EBIT fell 13% in the last year. If things keep going like that, handling the debt will about as easy as bundling an angry house cat into its travel box. When analysing debt levels, the balance sheet is the obvious place to start. But you can’t view debt in total isolation; since Key Tronic will need earnings to service that debt.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Over the last three years, Key Tronic saw substantial negative free cash flow, in total. While that may be a result of expenditure for growth, it does make the debt far more risky.

Our View

On the face of it, Key Tronic’s conversion of EBIT to free cash flow left us tentative about the stock, and its level of total liabilities was no more enticing than the one empty restaurant on the busiest night of the year. And furthermore, its interest cover also fails to instill confidence. Considering everything we’ve mentioned above, it’s fair to say that Key Tronic is carrying heavy debt load. If you play with fire you risk getting burnt, so we’d probably give this stock a wide berth. The balance sheet is clearly the area to focus on when you are analysing debt.