Legendary fund manager Li Lu (who Charlie Munger backed) once said, ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, General Mills, Inc. (NYSE:GIS) does carry debt. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

How Much Debt Does General Mills Carry?

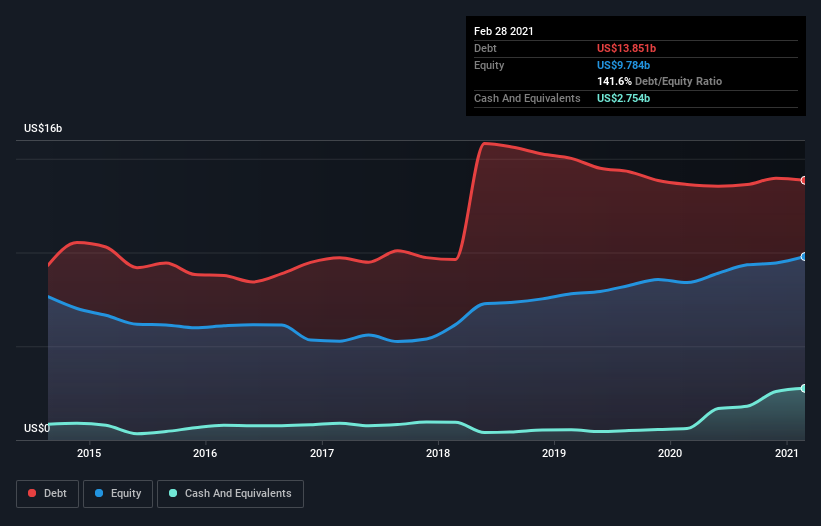

As you can see below, General Mills had US$13.5b of debt, at February 2021, which is about the same as the year before. You can click the chart for greater detail. On the flip side, it has US$2.75b in cash leading to net debt of about US$10.7b.

How Strong Is General Mills’ Balance Sheet?

The latest balance sheet data shows that General Mills had liabilities of US$9.59b due within a year, and liabilities of US$13.3b falling due after that. Offsetting these obligations, it had cash of US$2.75b as well as receivables valued at US$1.78b due within 12 months. So its liabilities total US$18.3b more than the combination of its cash and short-term receivables.

This deficit isn’t so bad because General Mills is worth a massive US$36.7b, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. But it’s clear that we should definitely closely examine whether it can manage its debt without dilution.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

General Mills has net debt to EBITDA of 2.6 suggesting it uses a fair bit of leverage to boost returns. On the plus side, its EBIT was 8.2 times its interest expense, and its net debt to EBITDA, was quite high, at 2.6. If General Mills can keep growing EBIT at last year’s rate of 18% over the last year, then it will find its debt load easier to manage. There’s no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if General Mills can strengthen its balance sheet over time.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So we always check how much of that EBIT is translated into free cash flow. Over the last three years, General Mills recorded free cash flow worth a fulsome 82% of its EBIT, which is stronger than we’d usually expect. That puts it in a very strong position to pay down debt.

Our View

The good news is that General Mills’s demonstrated ability to convert EBIT to free cash flow delights us like a fluffy puppy does a toddler. But, on a more sombre note, we are a little concerned by its level of total liabilities. All these things considered, it appears that General Mills can comfortably handle its current debt levels. Of course, while this leverage can enhance returns on equity, it does bring more risk, so it’s worth keeping an eye on this one. When analysing debt levels, the balance sheet is the obvious place to start.