David Iben put it well when he said, ‘Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. Importantly, Johnson Controls International plc (NYSE:JCI) does carry debt. But the more important question is: how much risk is that debt creating?

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we think about a company’s use of debt, we first look at cash and debt together.

What Is Johnson Controls International’s Net Debt?

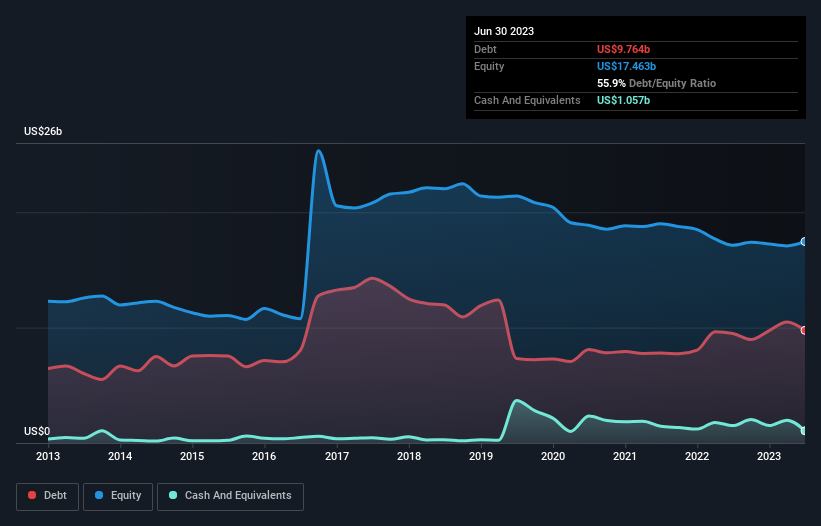

As you can see below, Johnson Controls International had US$9.76b of debt, at June 2023, which is about the same as the year before. You can click the chart for greater detail. However, because it has a cash reserve of US$1.06b, its net debt is less, at about US$8.71b.

How Healthy Is Johnson Controls International’s Balance Sheet?

We can see from the most recent balance sheet that Johnson Controls International had liabilities of US$11.1b falling due within a year, and liabilities of US$14.2b due beyond that. On the other hand, it had cash of US$1.06b and US$6.55b worth of receivables due within a year. So its liabilities total US$17.7b more than the combination of its cash and short-term receivables.

This deficit isn’t so bad because Johnson Controls International is worth a massive US$35.1b, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

We’d say that Johnson Controls International’s moderate net debt to EBITDA ratio ( being 2.4), indicates prudence when it comes to debt. And its strong interest cover of 10.7 times, makes us even more comfortable. If Johnson Controls International can keep growing EBIT at last year’s rate of 12% over the last year, then it will find its debt load easier to manage. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Johnson Controls International’s ability to maintain a healthy balance sheet going forward.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. Over the most recent three years, Johnson Controls International recorded free cash flow worth 61% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Our View

On our analysis Johnson Controls International’s interest cover should signal that it won’t have too much trouble with its debt. But the other factors we noted above weren’t so encouraging. For example, its level of total liabilities makes us a little nervous about its debt. Considering this range of data points, we think Johnson Controls International is in a good position to manage its debt levels. Having said that, the load is sufficiently heavy that we would recommend any shareholders keep a close eye on it.