David Iben put it well when he said, ‘Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. As with many other companies Amkor Technology, Inc. (NASDAQ:AMKR) makes use of debt. But is this debt a concern to shareholders?

What Risk Does Debt Bring?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

What Is Amkor Technology’s Debt?

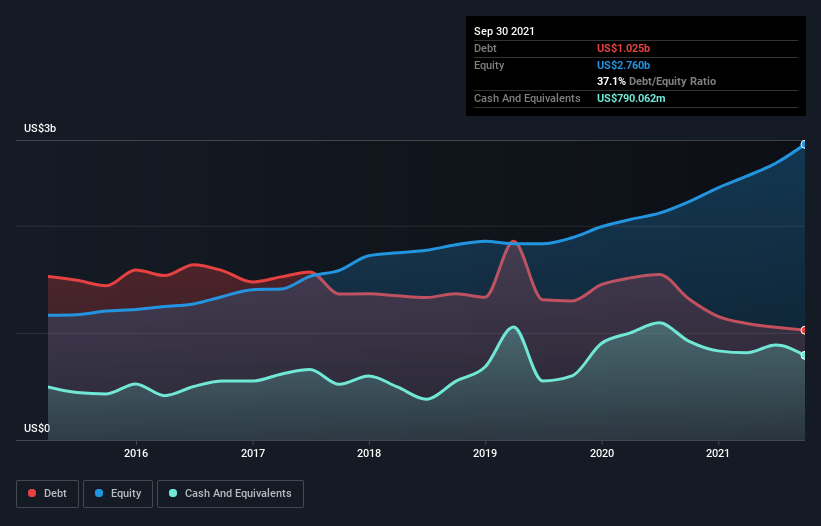

You can click the graphic below for the historical numbers, but it shows that Amkor Technology had US$1.02b of debt in September 2021, down from US$1.32b, one year before. However, it also had US$790.1m in cash, and so its net debt is US$234.6m.

How Healthy Is Amkor Technology’s Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Amkor Technology had liabilities of US$1.74b due within 12 months and liabilities of US$1.27b due beyond that. On the other hand, it had cash of US$790.1m and US$1.29b worth of receivables due within a year. So it has liabilities totalling US$931.1m more than its cash and near-term receivables, combined.

Given Amkor Technology has a market capitalization of US$5.80b, it’s hard to believe these liabilities pose much threat. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Amkor Technology’s net debt is only 0.19 times its EBITDA. And its EBIT covers its interest expense a whopping 13.2 times over. So we’re pretty relaxed about its super-conservative use of debt. In addition to that, we’re happy to report that Amkor Technology has boosted its EBIT by 60%, thus reducing the spectre of future debt repayments. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Amkor Technology can strengthen its balance sheet over time.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So it’s worth checking how much of that EBIT is backed by free cash flow. Looking at the most recent three years, Amkor Technology recorded free cash flow of 47% of its EBIT, which is weaker than we’d expect. That’s not great, when it comes to paying down debt.

Our View

Amkor Technology’s interest cover suggests it can handle its debt as easily as Cristiano Ronaldo could score a goal against an under 14’s goalkeeper. And the good news does not stop there, as its EBIT growth rate also supports that impression! Looking at the bigger picture, we think Amkor Technology’s use of debt seems quite reasonable and we’re not concerned about it. While debt does bring risk, when used wisely it can also bring a higher return on equity.