The external fund manager backed by Berkshire Hathaway’s Charlie Munger, Li Lu, makes no bones about it when he says ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. As with many other companies ViewRay, Inc. (NASDAQ:VRAY) makes use of debt. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we examine debt levels, we first consider both cash and debt levels, together.

How Much Debt Does ViewRay Carry?

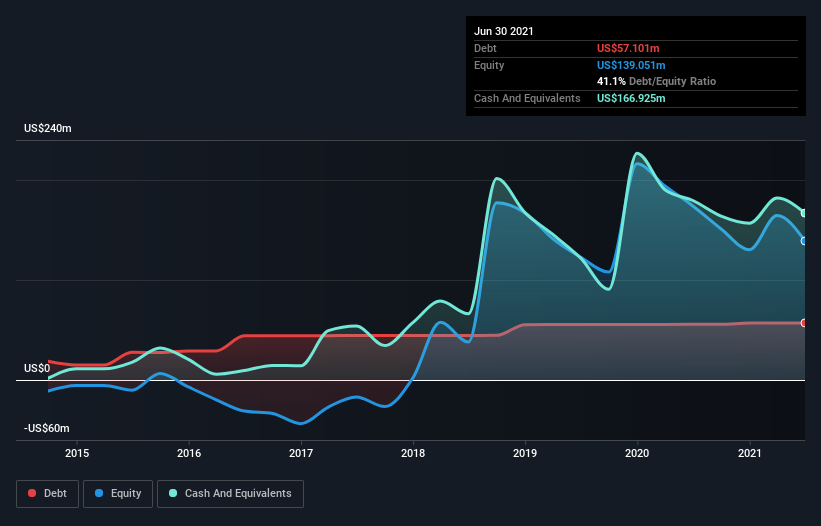

The chart below, which you can click on for greater detail, shows that ViewRay had US$57.1m in debt in June 2021; about the same as the year before. However, its balance sheet shows it holds US$166.9m in cash, so it actually has US$109.8m net cash.

A Look At ViewRay’s Liabilities

We can see from the most recent balance sheet that ViewRay had liabilities of US$53.0m falling due within a year, and liabilities of US$81.8m due beyond that. Offsetting these obligations, it had cash of US$166.9m as well as receivables valued at US$15.4m due within 12 months. So it actually has US$47.5m more liquid assets than total liabilities.

This surplus suggests that ViewRay has a conservative balance sheet, and could probably eliminate its debt without much difficulty. Succinctly put, ViewRay boasts net cash, so it’s fair to say it does not have a heavy debt load! There’s no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if ViewRay can strengthen its balance sheet over time.

Over 12 months, ViewRay made a loss at the EBIT level, and saw its revenue drop to US$59m, which is a fall of 10%. That’s not what we would hope to see.

So How Risky Is ViewRay?

By their very nature companies that are losing money are more risky than those with a long history of profitability. And in the last year ViewRay had an earnings before interest and tax (EBIT) loss, truth be told. Indeed, in that time it burnt through US$61m of cash and made a loss of US$112m. But at least it has US$109.8m on the balance sheet to spend on growth, near-term. Overall, its balance sheet doesn’t seem overly risky, at the moment, but we’re always cautious until we see the positive free cash flow. There’s no doubt that we learn most about debt from the balance sheet.