Warren Buffett famously said, ‘Volatility is far from synonymous with risk.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. Importantly, Tri Pointe Homes, Inc. (NYSE:TPH) does carry debt. But the more important question is: how much risk is that debt creating?

When Is Debt A Problem?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first step when considering a company’s debt levels is to consider its cash and debt together.

What Is Tri Pointe Homes’s Debt?

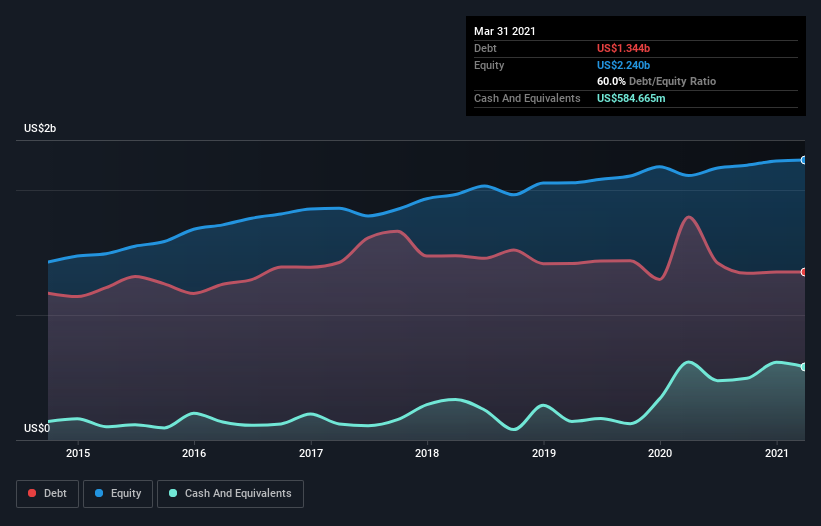

You can click the graphic below for the historical numbers, but it shows that Tri Pointe Homes had US$1.34b of debt in March 2021, down from US$1.78b, one year before. However, because it has a cash reserve of US$584.7m, its net debt is less, at about US$759.1m.

How Healthy Is Tri Pointe Homes’ Balance Sheet?

We can see from the most recent balance sheet that Tri Pointe Homes had liabilities of US$299.0m falling due within a year, and liabilities of US$1.55b due beyond that. Offsetting this, it had US$584.7m in cash and US$67.5m in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$1.20b.

Tri Pointe Homes has a market capitalization of US$2.93b, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. However, it is still worthwhile taking a close look at its ability to pay off debt.

In order to size up a company’s debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Tri Pointe Homes’s net debt to EBITDA ratio of about 1.6 suggests only moderate use of debt. And its commanding EBIT of 1k times its interest expense, implies the debt load is as light as a peacock feather. On top of that, Tri Pointe Homes grew its EBIT by 34% over the last twelve months, and that growth will make it easier to handle its debt. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Tri Pointe Homes’s ability to maintain a healthy balance sheet going forward. So if you’re focused on the future you can check out this free report showing analyst profit forecasts.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. Happily for any shareholders, Tri Pointe Homes actually produced more free cash flow than EBIT over the last three years. That sort of strong cash generation warms our hearts like a puppy in a bumblebee suit.

Our View

The good news is that Tri Pointe Homes’s demonstrated ability to cover its interest expense with its EBIT delights us like a fluffy puppy does a toddler. And that’s just the beginning of the good news since its conversion of EBIT to free cash flow is also very heartening. Zooming out, Tri Pointe Homes seems to use debt quite reasonably; and that gets the nod from us. After all, sensible leverage can boost returns on equity. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet.