David Iben put it well when he said, ‘Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. Importantly, IDEXX Laboratories, Inc. (NASDAQ:IDXX) does carry debt. But should shareholders be worried about its use of debt?

What Risk Does Debt Bring?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

How Much Debt Does IDEXX Laboratories Carry?

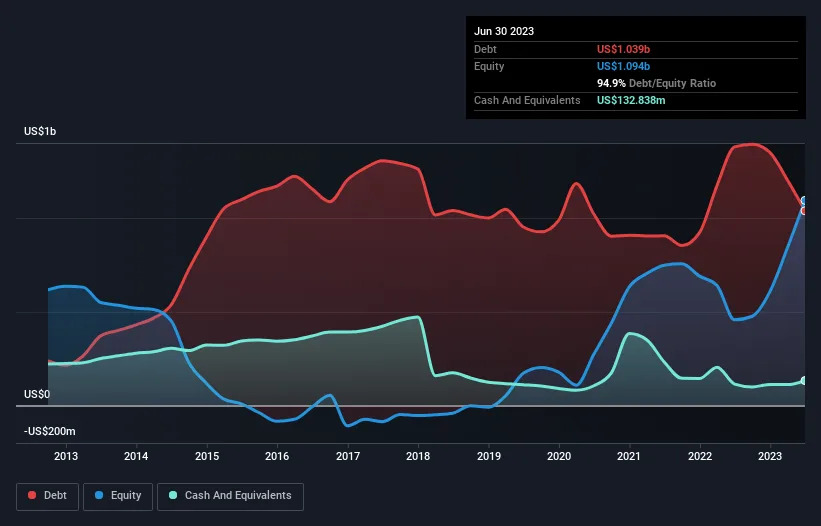

As you can see below, IDEXX Laboratories had US$1.04b of debt at June 2023, down from US$1.38b a year prior. However, it does have US$132.8m in cash offsetting this, leading to net debt of about US$905.7m.

How Healthy Is IDEXX Laboratories’ Balance Sheet?

We can see from the most recent balance sheet that IDEXX Laboratories had liabilities of US$883.9m falling due within a year, and liabilities of US$893.1m due beyond that. On the other hand, it had cash of US$132.8m and US$532.3m worth of receivables due within a year. So it has liabilities totalling US$1.11b more than its cash and near-term receivables, combined.

Of course, IDEXX Laboratories has a titanic market capitalization of US$40.9b, so these liabilities are probably manageable. Having said that, it’s clear that we should continue to monitor its balance sheet, lest it change for the worse.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

IDEXX Laboratories has a low net debt to EBITDA ratio of only 0.78. And its EBIT covers its interest expense a whopping 22.4 times over. So we’re pretty relaxed about its super-conservative use of debt. Another good sign is that IDEXX Laboratories has been able to increase its EBIT by 23% in twelve months, making it easier to pay down debt. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if IDEXX Laboratories can strengthen its balance sheet over time.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So we always check how much of that EBIT is translated into free cash flow. Over the most recent three years, IDEXX Laboratories recorded free cash flow worth 62% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Our View

The good news is that IDEXX Laboratories’s demonstrated ability to cover its interest expense with its EBIT delights us like a fluffy puppy does a toddler. And that’s just the beginning of the good news since its EBIT growth rate is also very heartening. It’s also worth noting that IDEXX Laboratories is in the Medical Equipment industry, which is often considered to be quite defensive. Overall, we don’t think IDEXX Laboratories is taking any bad risks, as its debt load seems modest. So the balance sheet looks pretty healthy, to us. The balance sheet is clearly the area to focus on when you are analysing debt.