The external fund manager backed by Berkshire Hathaway’s Charlie Munger, Li Lu, makes no bones about it when he says ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, Stride, Inc. (NYSE:LRN) does carry debt. But should shareholders be worried about its use of debt?

When Is Debt A Problem?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we examine debt levels, we first consider both cash and debt levels, together.

What Is Stride’s Net Debt?

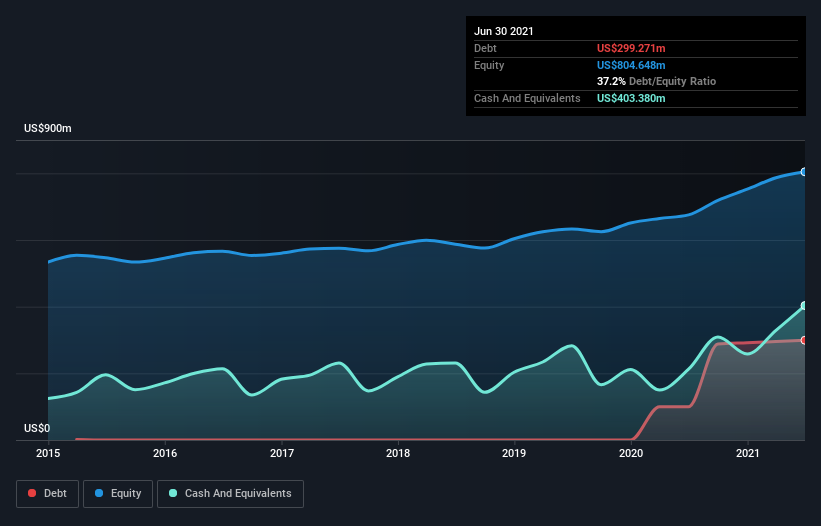

As you can see below, at the end of June 2021, Stride had US$299.3m of debt, up from US$100.0m a year ago. Click the image for more detail. However, it does have US$403.4m in cash offsetting this, leading to net cash of US$104.1m.

How Healthy Is Stride’s Balance Sheet?

We can see from the most recent balance sheet that Stride had liabilities of US$306.2m falling due within a year, and liabilities of US$466.4m due beyond that. On the other hand, it had cash of US$403.4m and US$369.3m worth of receivables due within a year. So these liquid assets roughly match the total liabilities.

This state of affairs indicates that Stride’s balance sheet looks quite solid, as its total liabilities are just about equal to its liquid assets. So it’s very unlikely that the US$1.48b company is short on cash, but still worth keeping an eye on the balance sheet. Simply put, the fact that Stride has more cash than debt is arguably a good indication that it can manage its debt safely.

Better yet, Stride grew its EBIT by 227% last year, which is an impressive improvement. If maintained that growth will make the debt even more manageable in the years ahead. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Stride’s ability to maintain a healthy balance sheet going forward.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. Stride may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. Happily for any shareholders, Stride actually produced more free cash flow than EBIT over the last three years. That sort of strong cash conversion gets us as excited as the crowd when the beat drops at a Daft Punk concert.

Summing up

While we empathize with investors who find debt concerning, you should keep in mind that Stride has net cash of US$104.1m, as well as more liquid assets than liabilities. And it impressed us with free cash flow of US$82m, being 107% of its EBIT.