Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that ‘Volatility is far from synonymous with risk.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. As with many other companies Chegg, Inc. (NYSE:CHGG) makes use of debt. But the real question is whether this debt is making the company risky.

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. The first step when considering a company’s debt levels is to consider its cash and debt together.

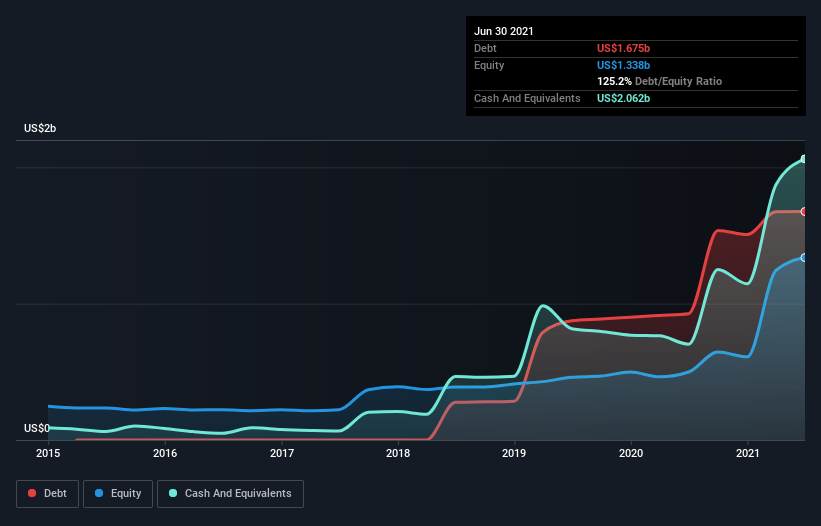

What Is Chegg’s Net Debt?

The image below, which you can click on for greater detail, shows that at June 2021 Chegg had debt of US$1.68b, up from US$926.2m in one year. But on the other hand it also has US$2.06b in cash, leading to a US$386.4m net cash position.

How Healthy Is Chegg’s Balance Sheet?

The latest balance sheet data shows that Chegg had liabilities of US$113.5m due within a year, and liabilities of US$1.70b falling due after that. Offsetting these obligations, it had cash of US$2.06b as well as receivables valued at US$10.1m due within 12 months. So it can boast US$258.7m more liquid assets than total liabilities.

This short term liquidity is a sign that Chegg could probably pay off its debt with ease, as its balance sheet is far from stretched. Succinctly put, Chegg boasts net cash, so it’s fair to say it does not have a heavy debt load!

Notably, Chegg’s EBIT launched higher than Elon Musk, gaining a whopping 124% on last year. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Chegg’s ability to maintain a healthy balance sheet going forward.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. While Chegg has net cash on its balance sheet, it’s still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. Over the last three years, Chegg actually produced more free cash flow than EBIT. There’s nothing better than incoming cash when it comes to staying in your lenders’ good graces.

Summing up

While we empathize with investors who find debt concerning, you should keep in mind that Chegg has net cash of US$386.4m, as well as more liquid assets than liabilities. The cherry on top was that in converted 226% of that EBIT to free cash flow, bringing in US$149m. So is Chegg’s debt a risk? It doesn’t seem so to us. There’s no doubt that we learn most about debt from the balance sheet.