David Iben put it well when he said, ‘Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, Southwest Airlines Co. (NYSE:LUV) does carry debt. But the real question is whether this debt is making the company risky.

What Risk Does Debt Bring?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we think about a company’s use of debt, we first look at cash and debt together.

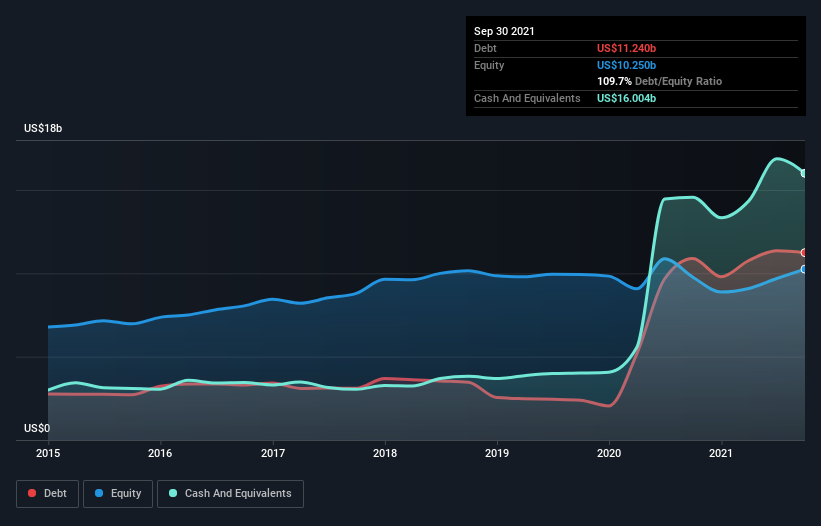

What Is Southwest Airlines’s Net Debt?

The chart below, which you can click on for greater detail, shows that Southwest Airlines had US$11.2b in debt in September 2021; about the same as the year before. However, it does have US$16.0b in cash offsetting this, leading to net cash of US$4.76b.

A Look At Southwest Airlines’ Liabilities

The latest balance sheet data shows that Southwest Airlines had liabilities of US$9.14b due within a year, and liabilities of US$17.7b falling due after that. Offsetting these obligations, it had cash of US$16.0b as well as receivables valued at US$1.48b due within 12 months. So it has liabilities totalling US$9.38b more than its cash and near-term receivables, combined.https://81457f54336f89368bcc838fb6a6702e.safeframe.googlesyndication.com/safeframe/1-0-38/html/container.html

This deficit isn’t so bad because Southwest Airlines is worth a massive US$26.6b, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. But it’s clear that we should definitely closely examine whether it can manage its debt without dilution. While it does have liabilities worth noting, Southwest Airlines also has more cash than debt, so we’re pretty confident it can manage its debt safely. There’s no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Southwest Airlines can strengthen its balance sheet over time.

Over 12 months, Southwest Airlines saw its revenue hold pretty steady, and it did not report positive earnings before interest and tax. While that hardly impresses, its not too bad either.

So How Risky Is Southwest Airlines?

Although Southwest Airlines had an earnings before interest and tax (EBIT) loss over the last twelve months, it made a statutory profit of US$1.0m. So taking that on face value, and considering the cash, we don’t think its very risky in the near term. With revenue growth uninspiring, we’d really need to see some positive EBIT before mustering much enthusiasm for this business. The balance sheet is clearly the area to focus on when you are analysing debt.