Howard Marks put it nicely when he said that, rather than worrying about share price volatility, ‘The possibility of permanent loss is the risk I worry about… and every practical investor I know worries about.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. As with many other companies e.l.f. Beauty, Inc. (NYSE:ELF) makes use of debt. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we examine debt levels, we first consider both cash and debt levels, together.

What Is e.l.f. Beauty’s Net Debt?

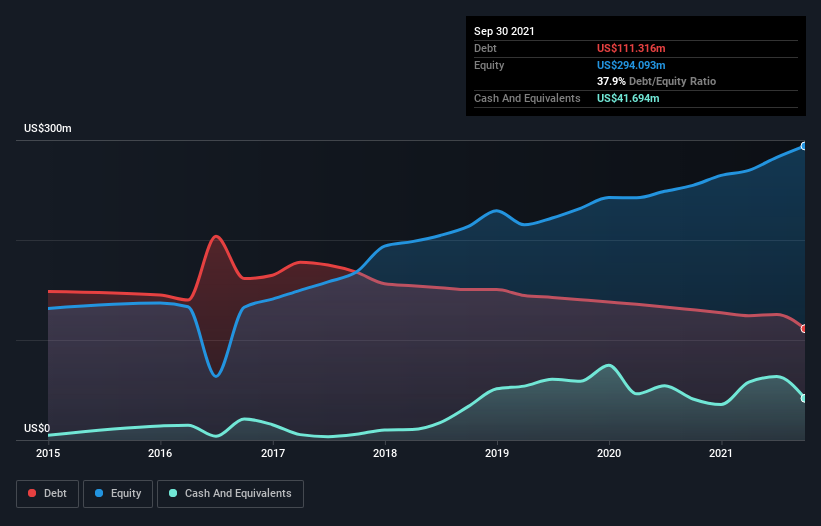

You can click the graphic below for the historical numbers, but it shows that e.l.f. Beauty had US$111.3m of debt in September 2021, down from US$130.2m, one year before. However, it also had US$41.7m in cash, and so its net debt is US$69.6m.

How Strong Is e.l.f. Beauty’s Balance Sheet?

According to the last reported balance sheet, e.l.f. Beauty had liabilities of US$71.2m due within 12 months, and liabilities of US$127.7m due beyond 12 months. Offsetting these obligations, it had cash of US$41.7m as well as receivables valued at US$44.4m due within 12 months. So it has liabilities totalling US$112.9m more than its cash and near-term receivables, combined.https://29935bb9c31ed38a47b0279d149c35b7.safeframe.googlesyndication.com/safeframe/1-0-38/html/container.html

Of course, e.l.f. Beauty has a market capitalization of US$1.62b, so these liabilities are probably manageable. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

With net debt sitting at just 1.5 times EBITDA, e.l.f. Beauty is arguably pretty conservatively geared. And this view is supported by the solid interest coverage, with EBIT coming in at 8.4 times the interest expense over the last year. On top of that, e.l.f. Beauty grew its EBIT by 36% over the last twelve months, and that growth will make it easier to handle its debt. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if e.l.f. Beauty can strengthen its balance sheet over time.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So it’s worth checking how much of that EBIT is backed by free cash flow. Over the last three years, e.l.f. Beauty actually produced more free cash flow than EBIT. That sort of strong cash generation warms our hearts like a puppy in a bumblebee suit.

Our View

The good news is that e.l.f. Beauty’s demonstrated ability to convert EBIT to free cash flow delights us like a fluffy puppy does a toddler. And that’s just the beginning of the good news since its EBIT growth rate is also very heartening. Considering this range of factors, it seems to us that e.l.f. Beauty is quite prudent with its debt, and the risks seem well managed. So we’re not worried about the use of a little leverage on the balance sheet. When analysing debt levels, the balance sheet is the obvious place to start.