Warren Buffett famously said, ‘Volatility is far from synonymous with risk.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. Importantly, SI-BONE, Inc. (NASDAQ:SIBN) does carry debt. But the more important question is: how much risk is that debt creating?

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

What Is SI-BONE’s Debt?

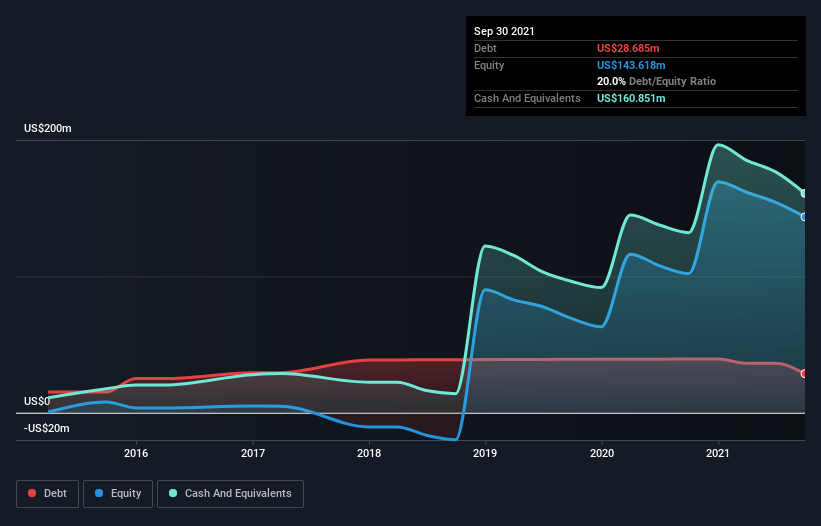

You can click the graphic below for the historical numbers, but it shows that SI-BONE had US$28.7m of debt in September 2021, down from US$39.4m, one year before. However, its balance sheet shows it holds US$160.9m in cash, so it actually has US$132.2m net cash.

How Healthy Is SI-BONE’s Balance Sheet?

We can see from the most recent balance sheet that SI-BONE had liabilities of US$14.6m falling due within a year, and liabilities of US$35.8m due beyond that. Offsetting these obligations, it had cash of US$160.9m as well as receivables valued at US$12.6m due within 12 months. So it actually has US$123.1m more liquid assets than total liabilities.

It’s good to see that SI-BONE has plenty of liquidity on its balance sheet, suggesting conservative management of liabilities. Due to its strong net asset position, it is not likely to face issues with its lenders. Simply put, the fact that SI-BONE has more cash than debt is arguably a good indication that it can manage its debt safely. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if SI-BONE can strengthen its balance sheet over time.

Over 12 months, SI-BONE reported revenue of US$87m, which is a gain of 23%, although it did not report any earnings before interest and tax. With any luck the company will be able to grow its way to profitability.

So How Risky Is SI-BONE?

Statistically speaking companies that lose money are riskier than those that make money. And we do note that SI-BONE had an earnings before interest and tax (EBIT) loss, over the last year. Indeed, in that time it burnt through US$40m of cash and made a loss of US$51m. But the saving grace is the US$132.2m on the balance sheet. That kitty means the company can keep spending for growth for at least two years, at current rates. SI-BONE’s revenue growth shone bright over the last year, so it may well be in a position to turn a profit in due course. Pre-profit companies are often risky, but they can also offer great rewards. The balance sheet is clearly the area to focus on when you are analysing debt.