The external fund manager backed by Berkshire Hathaway’s Charlie Munger, Li Lu, makes no bones about it when he says ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We can see that Sientra, Inc. (NASDAQ:SIEN) does use debt in its business. But should shareholders be worried about its use of debt?

What Risk Does Debt Bring?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we think about a company’s use of debt, we first look at cash and debt together.

How Much Debt Does Sientra Carry?

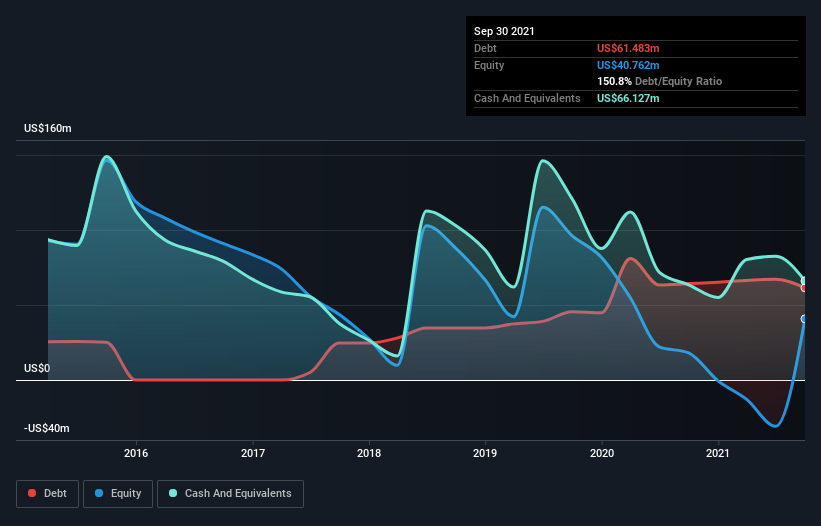

The image below, which you can click on for greater detail, shows that Sientra had debt of US$61.5m at the end of September 2021, a reduction from US$64.3m over a year. But on the other hand it also has US$66.1m in cash, leading to a US$4.64m net cash position.

How Strong Is Sientra’s Balance Sheet?

According to the last reported balance sheet, Sientra had liabilities of US$71.7m due within 12 months, and liabilities of US$74.2m due beyond 12 months. On the other hand, it had cash of US$66.1m and US$26.6m worth of receivables due within a year. So its liabilities total US$53.2m more than the combination of its cash and short-term receivables.

This deficit isn’t so bad because Sientra is worth US$201.1m, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk. Despite its noteworthy liabilities, Sientra boasts net cash, so it’s fair to say it does not have a heavy debt load! When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Sientra’s ability to maintain a healthy balance sheet going forward.

In the last year Sientra wasn’t profitable at an EBIT level, but managed to grow its revenue by 53%, to US$92m. With any luck the company will be able to grow its way to profitability.

So How Risky Is Sientra?

We have no doubt that loss making companies are, in general, riskier than profitable ones. And the fact is that over the last twelve months Sientra lost money at the earnings before interest and tax (EBIT) line. Indeed, in that time it burnt through US$43m of cash and made a loss of US$90m. However, it has net cash of US$4.64m, so it has a bit of time before it will need more capital. With very solid revenue growth in the last year, Sientra may be on a path to profitability. By investing before those profits, shareholders take on more risk in the hope of bigger rewards.